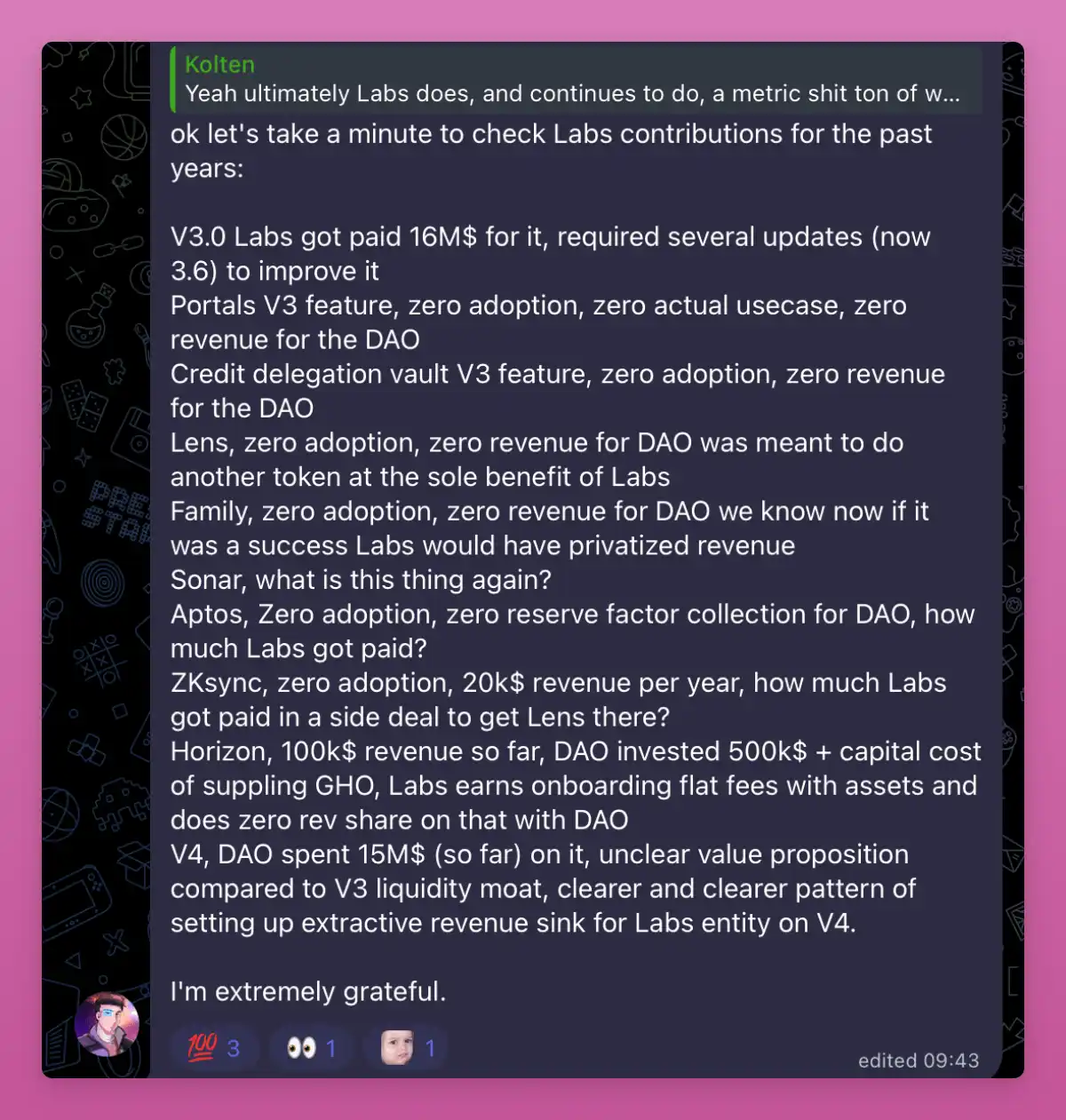

Yearly $10M Loss in Revenue Triggers Governance Dispute, Aave Labs Accused of 'DAO Treachery'

Aave Labs and Aave DAO's conflict regarding frontend integration and fee ownership fundamentally revolves around questioning a core issue: the control and distribution of the value created by the protocol.

Original Article Title: Who Owns 'Aave': Aave Labs vs Aave DAO

Original Article Author: Ignas, Crypto KOL

Original Article Translation: Felix, PANews

Recently, Aave Labs and Aave DAO engaged in a heated debate surrounding the fee allocation issue stemming from the CoWSwap integration. This debate has also been seen by the community as a potential crisis in DeFi governance. The author of this article interprets this debate from a neutral perspective, and the following details the content.

On December 4th, the lending protocol Aave Labs switched the default exchange integration of its front-end interface aave.com from ParaSwap to CoWSwap. While this may seem like a minor product update, it actually exposed a deep-seated conflict within Aave.

This conflict is not about CowSwap, fees, or user experience, but about ownership. Specifically, it is about who controls Aave, who decides on allocation, and who captures the value created around the protocol.

In the previous setup, the exchange feature primarily served the purpose of user retention:

Users could rearrange or exchange assets without leaving the Aave interface. Importantly, all referral fees or positive slippage surplus fees were redistributed as revenue to the Aave DAO treasury.

CowSwap's integration changed this dynamic.

According to Aave's documentation, exchanges now incur a fee of approximately 15 to 25 basis points. Orbit on behalf of EzR3aL (Note: a senior governance participant of Aave DAO and an independent delegate) investigated the destination of these fees and concluded: these fees no longer flow into the DAO treasury but instead into an address controlled by Aave Labs.

"Assuming a mere 200,000 USD is transferred weekly, the DAO loses at least 10 million USD per year." — EzR3aL

Did Aave Labs unilaterally sever the DAO's revenue source and transfer it to a private company?

Aave has successfully operated over the years because despite the blurred lines of responsibilities, all parties' interests remained aligned.

· DAO Governance Protocol

· Aave Labs Building Frontend Interface

Funds mostly flowed in one direction, so nobody paid much attention to defining the issue.

But now, it seems this tacit coordination has been broken.

As Aave founder and CEO Stani.eth wrote:

· "At the time, Aave Labs decided to donate to the Aave DAO in those cases (funds that could also be returned to users)"

Aave Labs' response: "The protocol and the product are different concepts."

A response from Aave Labs on the forum:

· "The frontend interface is operated by Aave Labs, entirely independent from the protocol and DAO management."

· "The frontend interface is a product, not a protocol component."

From their perspective, this is normal. Running a frontend requires funds, security requires funds, and support also requires funds.

The surplus from Paraswap flowing to the DAO is not a permanent rule. There is no precedent to follow.

ACI (a service provider serving the Aave DAO) and its founder Marc Zeller believe this is an issue of trust.

"Every service provider on the Aave DAO payroll has a mandatory fiduciary obligation to the DAO, and thus to the best interest of AAVE token holders." —Marc Zeller in a forum comment.

He believes there was an understanding: the DAO lends its brand and intellectual property, so the frontend's profits should also belong to the DAO. "It seems we have been fooled for a long time, thinking this was a given."

Marc Zeller also claims that the DAO has lost income, and routing decisions could push volume to competitors, resulting in Aave DAO losing about 10% of potential income.

Protocol vs. Product

Aave Labs has drawn a clear line between protocol and product.

The DAO manages the protocol and its on-chain economy. Aave Labs operates the frontend interface as an independent product with its own vision.

Just as explained by the Aave founder in this tweet:

· Aave Labs' frontend interface is a product that fully embodies our own principles, which we have been developing for over 8 years, similar to other interfaces using the Aave protocol, such as DeFi Saver.

· It is completely reasonable for Aave Labs to profit from its product, especially since it does not touch the protocol itself, and given the ByBit security incident, this ensures secure access to the protocol.

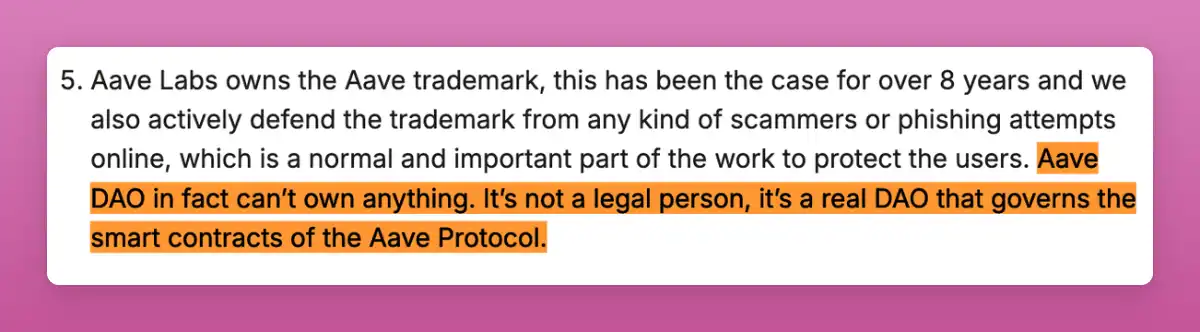

The Aave DAO does not own intellectual property rights because a DAO is not a legal entity and cannot hold trademarks or enforce them in court.

The DAO manages the smart contracts and on-chain parameters of the Aave protocol, but does not manage the brand itself.

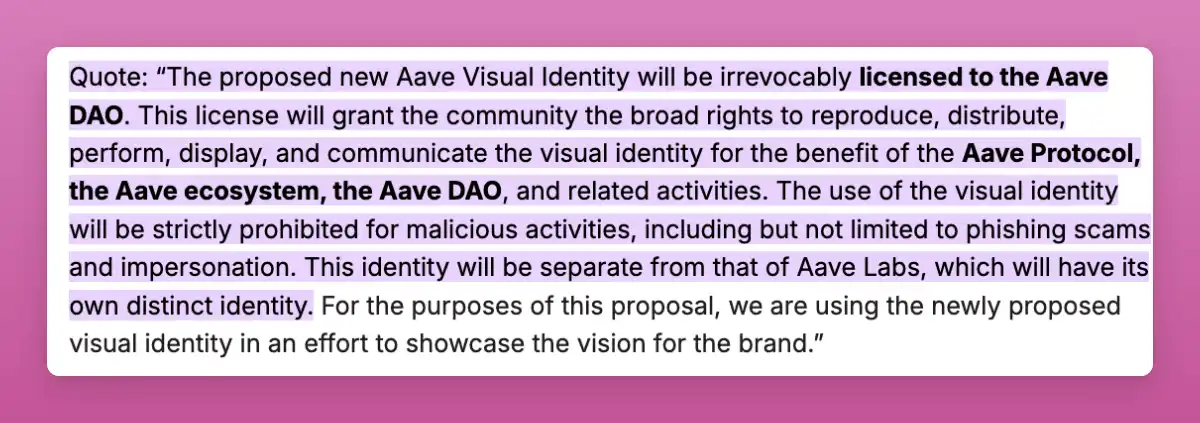

However, the DAO has been granted a license to use the Aave brand and visual identity for protocol-related purposes. Past governance proposals have explicitly granted the DAO broad rights to use the visual identity for "the benefit of the Aave protocol, Aave ecosystem, and Aave DAO."

Source: Aave

As EzR3aL puts it:

"The reason why charging this fee is feasible is because the Aave brand is well-known and accepted in the ecosystem. This is the brand that the Aave DAO paid for."

The value of the Aave brand does not originate from a logo.

Its value comes from:

· The DAO prudently managing risk

· Token holders bearing protocol risk

· The DAO paying fees to service providers

· The DAO surviving multiple crises without collapsing

· The protocol earning a reputation for being secure and reliable

This is what EzR3aL refers to as the "brand that the DAO paid for."

It's not a legal sense of payment, but an economic sense of payment, involving funds, governance, risk, and time.

Does this sound familiar?

Once again, it came back to the issue of Uniswap Labs and the Foundation regarding a similar matter about Uniswap's front-end fee. Ultimately, Uniswap restructured the equity and tokenholder rights, completely eliminating the front-end fee.

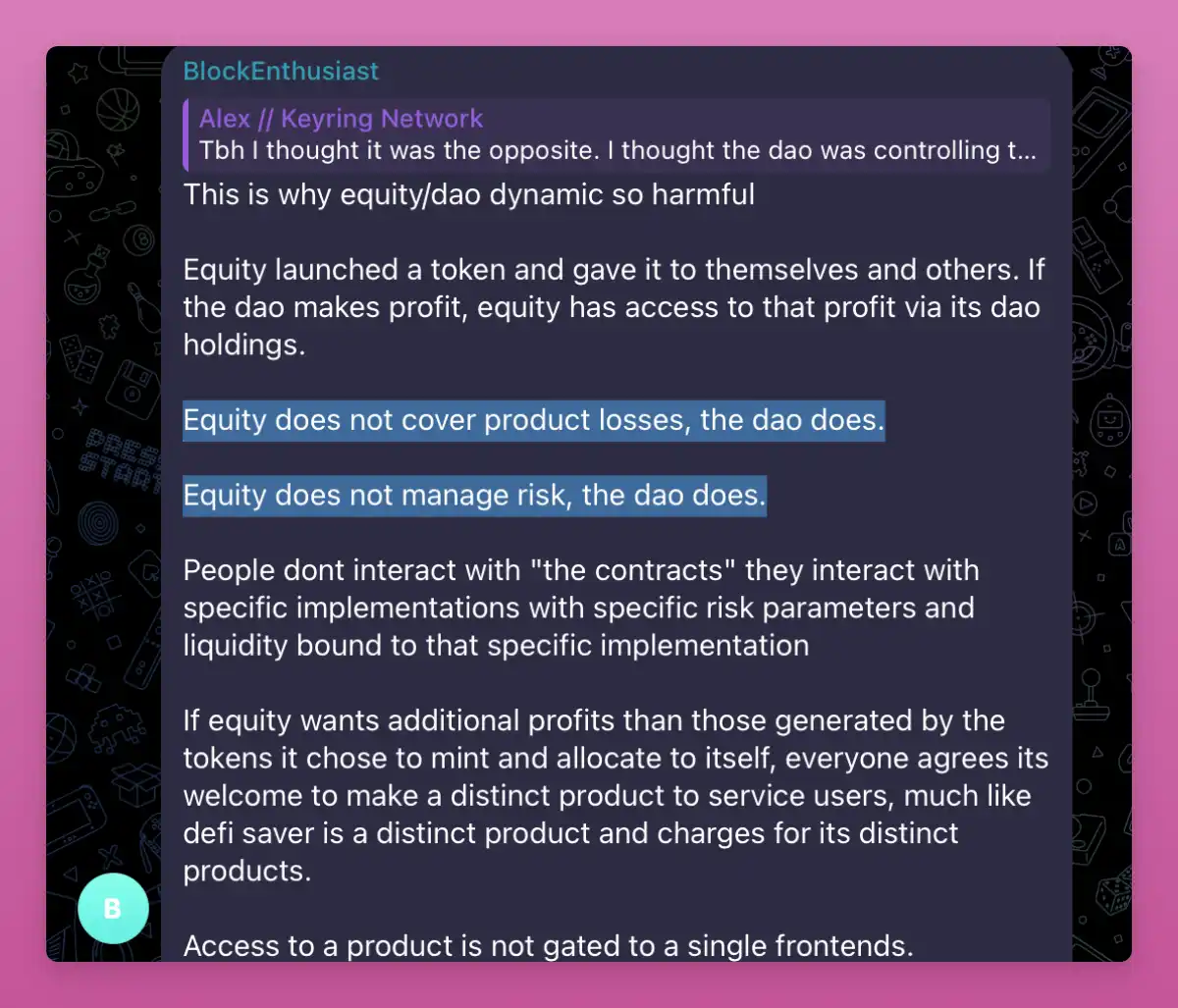

This is why the Equity/DAO dynamic can be harmful (as I discovered from the group chat).

The content in the image is as follows:

“The Equity issued a token and distributed these tokens to themselves and others. If the DAO generates a profit, Equity can receive a share of the profit through the tokens it holds in the DAO.

· However, Equity does not bear the product's losses, which are borne by the DAO.

· Equity also does not manage risk; risk management is the responsibility of the DAO.

Users do not directly interact with the ‘contract’ but with a specific implementation version that has specific risk parameters and liquidity tied to that specific implementation.

If Equity wants to earn additional returns beyond the profit generated from the tokens it initially minted and distributed to itself, everyone agrees it is free to develop a standalone product to provide services to users, just like DeFi Saver is a standalone product that charges for its unique services.

Access to a product should not be restricted to a single front end.”

At the time of writing, Aave Labs only acknowledged the critics' viewpoint on communication.

· What is genuinely valid criticism here is the communication or rather lack thereof.

Things were complicated enough, and now they are even worse.

Aave Labs proposed Horizon as a dedicated RWA instance.

Initially, the proposal included something that immediately raised concerns within the DAO: a new token with a diminishing profit share.

Representatives of various factions strongly opposed this (including the author), believing that introducing a separate token would dilute AAVE's value proposition and disrupt consensus.

The DAO emerged victorious, and Aave Labs was forced to concede. The new token plan was scrapped.

But this has sparked even greater division.

Despite numerous concerns (one of which specifically points out the clear responsibilities of Aave Labs versus the DAO), Horizon still went live. This was the most controversial vote to win.

I voted against deployment, advocating for a friendly agreement to avoid future conflict escalation. And that is exactly the current situation. The economic issue rapidly became the focal point of the conflict.

According to data cited by Marc Zeller, so far, Horizon has generated about $100,000 in total revenue, while the Aave DAO has put in $500,000 of incentive funds, making its net assets approximately -$400,000.

And this is not even taking into account other factors.

Marc also points out that tens of millions of GHO tokens have been invested in Horizon, but the earnings are insufficient to cover the costs required to maintain the GHO pegged price.

If these opportunity costs are factored in, the DAO's true economic situation could be even worse.

This prompted ACI to raise an issue beyond Horizon itself:

If a project funded by a DAO has directly poor economic performance, is that the whole story?

Or, are there additional benefits, integration fees, or off-chain arrangements that token holders are not seeing?

Over the years, deployments and plans proposed by various Labs have ultimately led to the DAO's costs exceeding its returns.

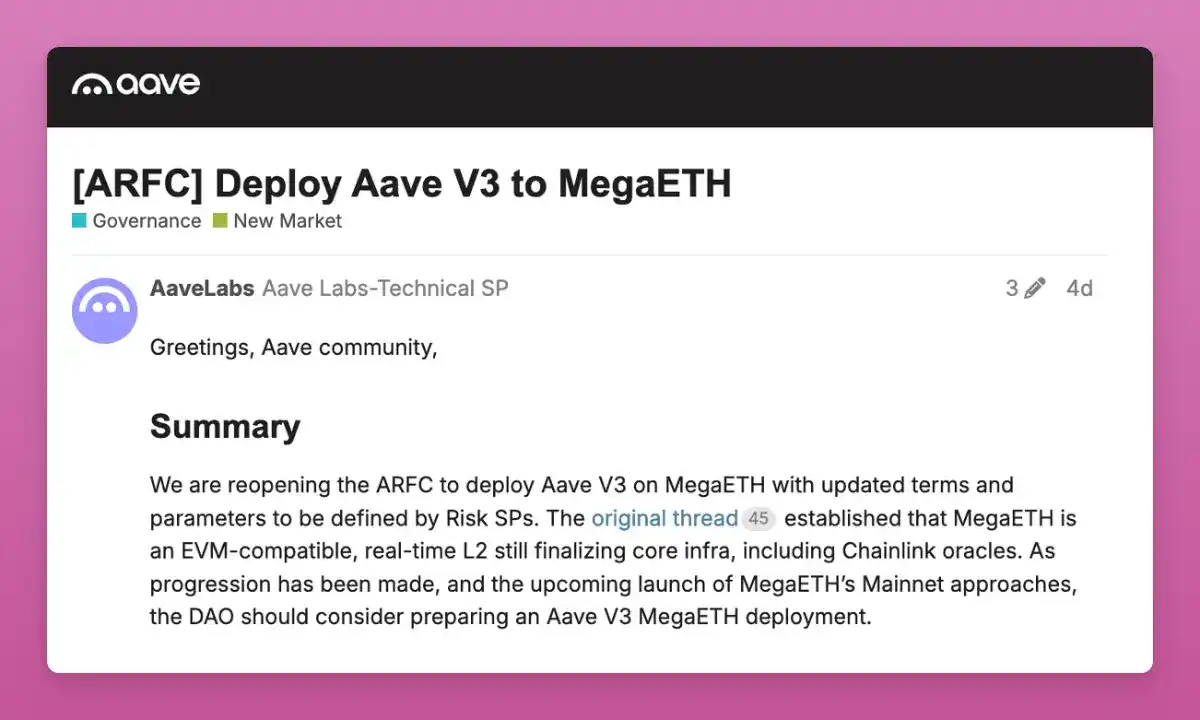

A few days after Aave Labs proposed a DAO motion to deploy Aave V3 on MegaETH, discussions on the matter ensued.

In return, "Aave Labs will receive 30 million points from MegaETH."

Then, "These points may be distributed as incentives on the Aave V3 MegaETH market following Aave DAO's GTM strategy."

The issue lies in the transparency and ensuring that incentives are distributed as agreed upon when a product is operated by a private entity using DAO-backed assets.

Source: Aave

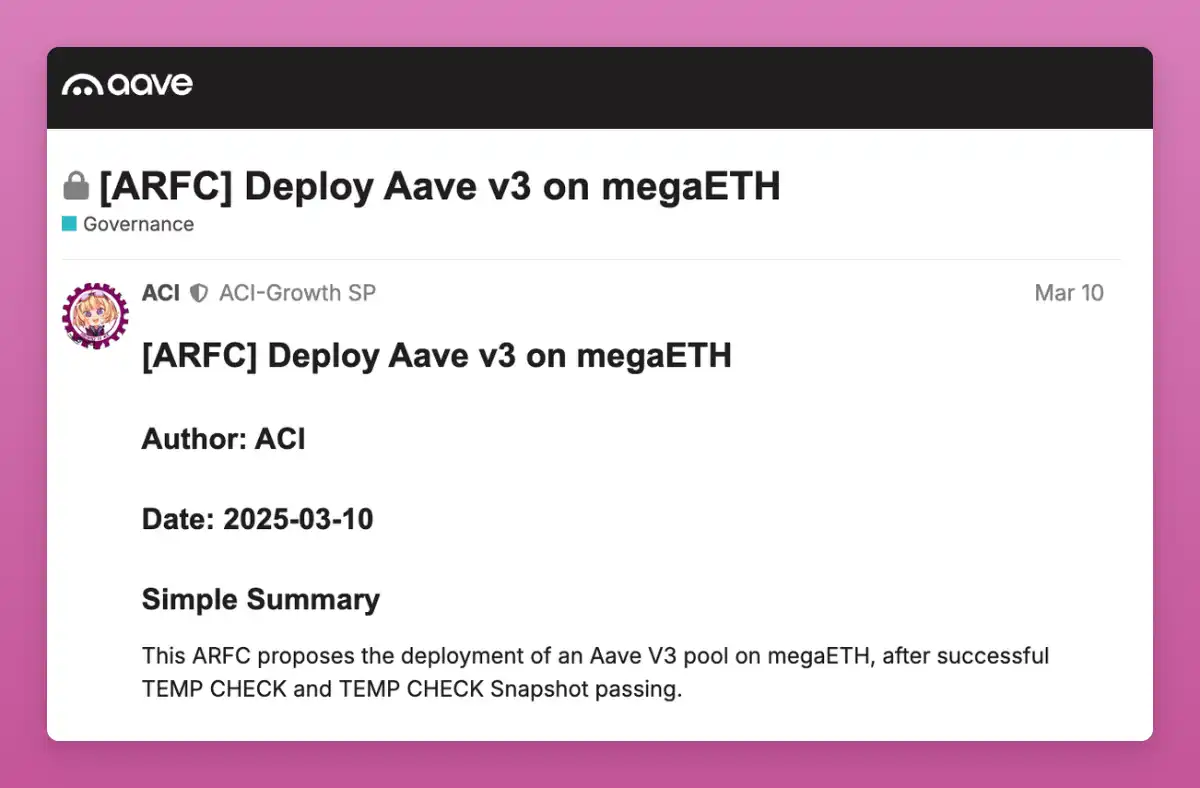

The surprising aspect of this proposal has another reason:

The Aave DAO has collaborated with multiple service providers, especially ACI, proposing deployment on MegaETH as early as March. Relevant discussions are still ongoing.

Source: Aave

As Marc commented on the forum:

“During the discussion, we were very surprised to find that Aave Labs decided to bypass all precedents, abandon all ongoing progress, and reach out directly to MegaETH. We only learned of this when the proposal was posted on the forum.”

Treasury

Another part of this debate concerns the Aave Treasury.

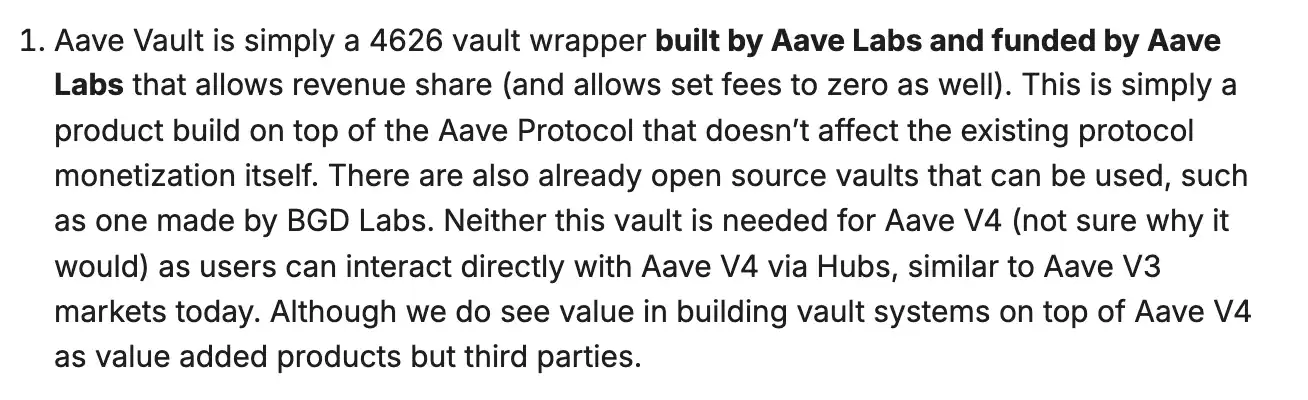

The Aave Treasury is an application-level product built and funded by Aave Labs. Technically, they are ERC-4626 Treasury Wrappers built on top of the Aave protocol to abstract position management for users.

Stani explained this very clearly:

“The Aave Treasury is just a 4626 Treasury Wrapper built and funded by Aave Labs.”

From the perspective of Aave Labs, this should not be controversial.

The Treasuries are not protocol components. They do not affect the protocol's revenue.

They are optional, and users can always interact directly with the Aave markets or use third-party Treasuries.

· “For Aave V4, this Treasury is not mandatory… Users can interact with Aave V4 directly through Hubs.”

And since Treasuries are products, Aave Labs believes they are entitled to profit from them.

· “Aave Labs profiting from their products is entirely fine, especially since they do not involve the protocol itself.”

So why was the Treasury involved in this dispute?

The reason lies in the distribution channel.

If the Treasury becomes the default user experience of Aave V4, then a Labs-owned, Aave-branded product could serve as a bridge between users and the protocol, leveraging the reputation, liquidity, and trust built on the DAO to collect transaction fees.

Despite the increasing adoption of Aave's products, the AAVE token would still be impacted.

Once again, the author believes this issue falls into the same category as the dispute between Uniswap Labs and the Foundation regarding front-end products.

In summary, CowSwap, Horizon, MegaETH, and Aave Vaults all face the same issue.

Aave Labs sees itself as an independent builder, operating a subjective product on a neutral protocol.

The DAO increasingly perceives that the protocol's value is being realized beyond its direct control.

The Aave DAO does not own intellectual property, but it is authorized to use the Aave brand and visual identity for protocol-related purposes.

This dispute is crucial because the upcoming Aave v4 release is explicitly aimed at shifting complexity from the user side to the abstraction layer.

More routes, more automation, and more products between users and the core protocol.

More abstraction means more control over user experience, and user experience control is crucial for value creation/extraction.

This article strives to remain neutral. However, it is hoped that consensus can be reached regarding value capture for $AAVE token holders.

The consensus the author hopes to achieve is not only beneficial for Aave itself but also because Aave has set an important precedent for how equity and tokens can coexist.

Uniswap Labs has already gone through this process, ultimately benefiting $UNI holders.

Aave should do the same.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Clean Energy Market Fluidity: Ushering in a New Age with CFTC-Sanctioned Platforms

- REsurety's CleanTrade, the first CFTC-approved SEF for clean energy , is transforming market liquidity and transparency by standardizing VPPAs, PPAs, and RECs. - The platform attracted $16B in notional value within two months, enabling institutional investors to hedge energy risks while aligning with ESG goals through verifiable decarbonization metrics. - Renewable developers benefit from streamlined financing and securitization tools, creating predictable revenue streams and expanding access to capital

Investing in Human Capital for a Greener Tomorrow: The Growth of Education and Career Training in Renewable Energy

- Global energy transition drives rapid growth in renewable workforce demand, with U.S. wind turbine technician roles projected to surge 60.1% by 2033. - Institutions like Farmingdale State College bridge skill gaps through industry-aligned programs, offering hands-on training and partnerships with firms like Orsted and GE . - Investors gain strategic opportunities by funding vocational training and microcredentials, addressing decarbonization needs while boosting social equity through inclusive initiative

Clean Energy Market Fluidity: The CFTC-Endorsed Transformation

- CFTC approved CleanTrade as the first SEF for clean energy , addressing market fragmentation and liquidity gaps. - The platform enables institutional-scale trading of VPPAs and RECs with automated compliance and $16B in early trading volume. - Integrated analytics and regulatory compliance enhance transparency, reducing risks for investors in renewable energy assets. - Early adoption by Cargill and Mercuria highlights CleanTrade's potential to reshape $1.2T clean energy investment landscape.

How iRobot Strayed from Its Original Path