Global Crypto Regulation Era Begins as UK Implements OECD Disclosure Standards

- UK adopts OECD's CARF framework for crypto regulation, avoiding tax hikes but enforcing stricter compliance by 2026. - HMRC updates guidelines requiring crypto providers to report user data globally, aligning with 70+ countries' 2027 data exchange plans. - Compliance demands automated data collection, KYC upgrades, and penalties for non-compliance under new transparency rules. - Framework excludes self-custody wallets but covers major transactions, reshaping crypto's integration into global financial sys

The United Kingdom is moving toward tighter regulation of cryptocurrencies, though there are currently no plans to increase taxes on digital assets,

The UK’s rollout of CARF closely follows the OECD’s blueprint, with only minor local modifications. Under this framework, crypto service providers—including exchanges and brokers—must gather and submit user information, such as tax residency and transaction records, to HMRC. These reports will be shared across borders, strengthening global tax enforcement. The updated HMRC guidance highlights the consequences for inadequate due diligence, poor record-keeping, or late reporting, emphasizing the seriousness of the new regulatory requirements.

On a global scale, CARF marks a significant turning point for crypto oversight. Created by the OECD, the framework

While CARF’s coverage is extensive, it does not apply to all entities. Reporting obligations fall on exchanges, brokers, and platforms that facilitate crypto transactions, but self-custody wallets and non-commercial sites like CoinMarketCap are not included. Activities that must be reported include crypto-to-fiat conversions, wallet-to-wallet transfers, and retail payments over $50,000. Central bank digital currencies, certain forms of e-money, and NFTs that are purely collectibles are excluded from the framework.

To comply, crypto businesses will need to revamp their systems to automate data gathering, enhance KYC procedures, and submit annual reports. Companies must also revise onboarding processes and privacy policies to meet new regulatory demands. Legal professionals stress that preparing early is essential to avoid fines and operational setbacks, as CARF compliance is now a necessity for sustainable business operations.

The UK’s commitment to CARF demonstrates a worldwide trend of bringing crypto into the fold of regulated finance. Although the Gemini executive noted there are no new tax increases, the compliance responsibilities for service providers are significant. With the 2026 deadline drawing near, crypto companies must ensure they meet both UK and global standards to successfully adapt to these regulatory changes.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Hash Ribbon Flashes Signal That Often Marks Cyclical Bottoms for Bitcoin Price

Crypto for Advisors: Crypto’s Role in Portfolios

Bitcoin whale opens $56.7M Bitcoin long after 18 months on the sidelines

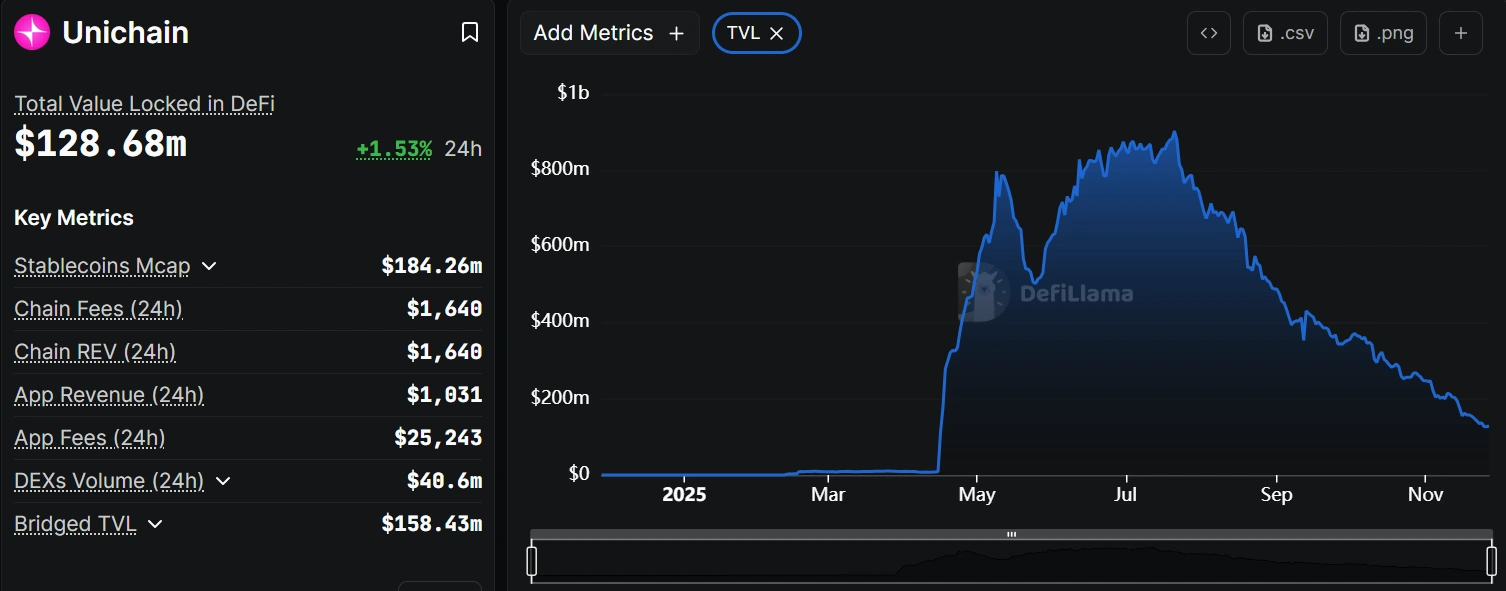

Unichain TVL collapses 86% as incentive program ends and liquidity exits