Written by: Santiago R Santos

Translated by: Luffy, Foresight News

Currently, everyone in the crypto industry is focused on the same headlines:

-

Exchange-Traded Funds (ETFs) have launched

-

Real-world companies are integrating stablecoins

-

Regulators are becoming increasingly friendly

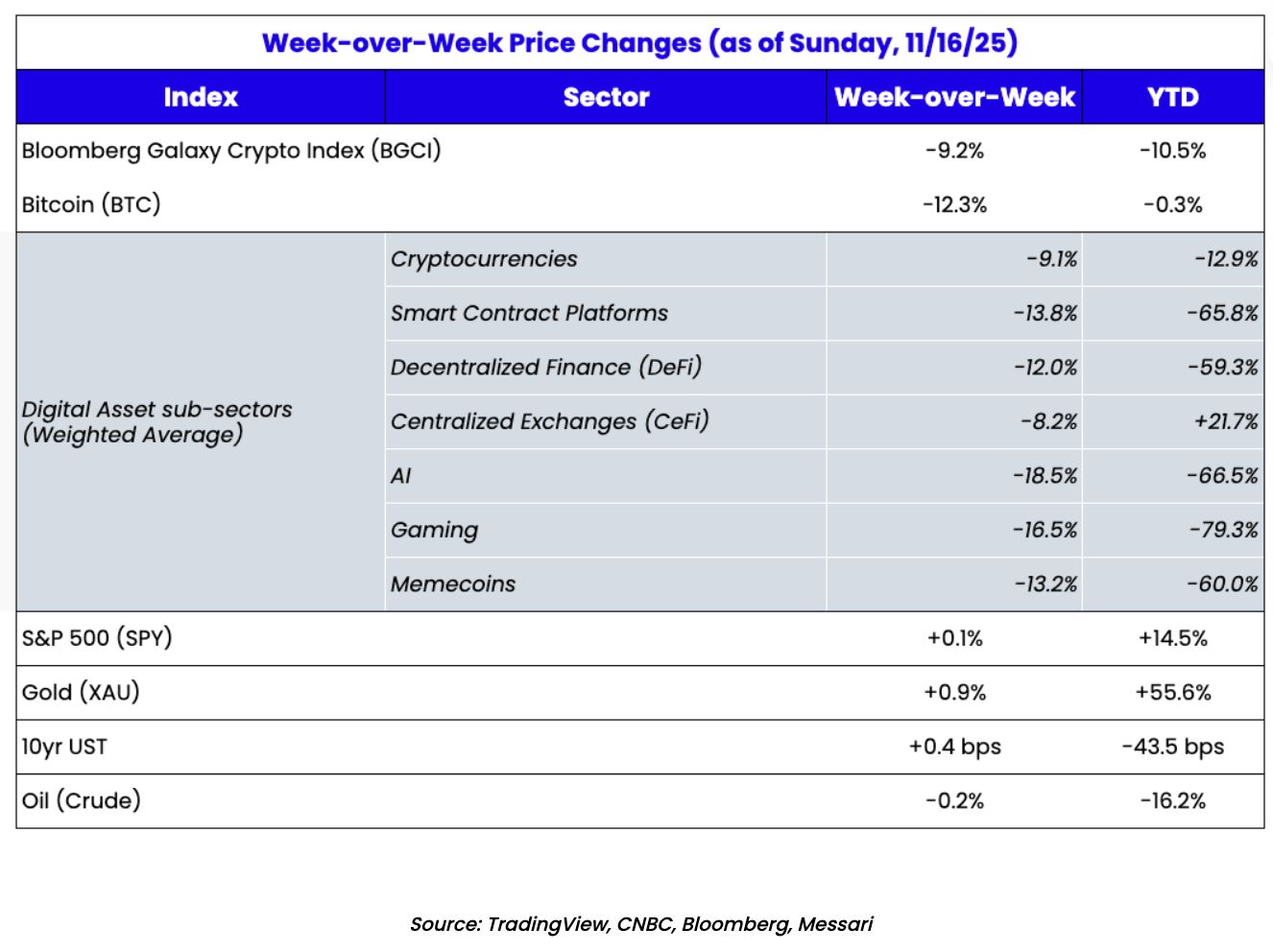

Aren’t these exactly what we once dreamed of? So why are prices still sluggish? Why has bitcoin been oscillating and giving back gains this year, while the US stock market is up 15%-20%? Why, even when “crypto is no longer a scam” has become mainstream consensus, are your favored altcoins still in the red?

Let’s have a real conversation about this issue.

Adoption ≠ Price Increase

There’s a deeply rooted assumption on crypto Twitter: “Once institutions enter, regulations are clear, JPMorgan issues tokens... we’ll skyrocket.”

Now, institutions are here, we’re making headlines, but crypto remains stagnant.

There’s really only one core question in investing: “Have these positives already been priced in?”

This is always the hardest thing to judge, but market behavior is sending a disturbing signal: we’ve gotten everything we wanted, yet prices haven’t moved up.

Could the market be inefficient? Of course. But why? Because most areas of the crypto industry have long been seriously disconnected from reality.

1.5 Trillion Dollar Market Cap... But Why?

Let’s zoom out. Bitcoin is in a league of its own, like gold—a perfect symbol of consensus. Currently, bitcoin’s market cap is about 1.9 trillion dollars, while gold’s is about 29 trillion dollars—bitcoin’s is less than 10% of gold’s. From a hedging and options value perspective, its logic is clear enough.

The total market cap of all other crypto assets—Ethereum, XRP, Solana, etc.—is about 1.5 trillion dollars, but the narrative behind them is much more fragile.

Today, no one doubts the potential of this technology, and few still think the whole industry is a scam—that phase has passed.

But potential doesn’t answer the real question: is an industry with only about 40 million active users really worth trillions of dollars?

Meanwhile, there are rumors that OpenAI’s IPO valuation is close to 1 trillion dollars, and its user base is about 20 times that of the entire crypto ecosystem.

Think carefully about this comparison. Moments like this force us to confront the core question: from now on, what’s the best way to gain crypto exposure?

Looking back at history: the answer is “infrastructure.” Early Ethereum, early Solana, early DeFi—these types of investments worked.

But what about now? The pricing of these assets seems to assume that future usage and fees will grow 100-fold. Perfect pricing, but with zero margin of safety.

The Market Isn’t Stupid, Just Greedy

This cycle has given us all the headlines we wanted... but some truths have also become clear:

-

The market doesn’t care about your narrative, only about the gap between price and fundamentals. If that gap persists, the market will eventually stop believing in you—especially when you start disclosing revenue data.

-

Crypto is no longer the hottest investment; artificial intelligence (AI) is. Capital chases trends—that’s how modern markets work. Right now, AI is the absolute star, and crypto is not.

-

Companies follow business logic, not ideology. Stripe launching the Tempo stablecoin is a warning sign. Perhaps companies won’t choose public chain infrastructure just because they heard on Bankless that “Ethereum is the world’s supercomputer”—they’ll only choose what benefits them most.

So, just because Larry Fink discovered that “crypto isn’t a scam,” does that mean your holdings will go up?

When assets are perfectly priced, a careless remark from Powell or a subtle expression from Jensen Huang can destroy the entire investment thesis.

Simple Math: Ethereum, Solana—Why Yield ≠ Profit?

Let’s roughly estimate the situation for mainstream L1 blockchains. First, staking yield (note: this is not profit):

-

Solana: About 419 million SOL staked, annualized yield about 6%, generating about 25 million SOL in staking rewards per year. At the current price of about $140 per SOL, the rewards are worth about $3.5 billion per year.

-

Ethereum: About 33.8 million ETH staked, annualized yield about 4%, generating about 1.35 million ETH in staking rewards per year. At the current price of about $3,100 per ETH, the rewards are worth about $4.2 billion per year.

Some see the staking data and say: “Look, stakers get yield! That’s value capture!”

No, staking rewards are not value capture. They are token inflation and dilution—the cost of network security, not profit.

True economic value = user-paid fees + tips + Maximum Extractable Value (MEV)—this is the closest thing to “profit” for blockchains.

From this perspective: in 2024, Ethereum generated about $2.7 billion in transaction fees, ranking first among all blockchains. Solana’s recent network revenue performance is leading, with hundreds of millions in quarterly revenue.

So, the current market situation is: Ethereum’s market cap is about $400 billion, with annual fee + MEV revenue of about $1-2 billion. This means, at peak cycle revenue, its price-to-sales ratio (note: PS = total market cap divided by main business revenue. The lower the PS, the greater the investment value of the stock) is as high as 200-400x.

Solana’s market cap is about $75-80 billion, with annualized revenue over $1 billion. Depending on the annualization method (note: don’t extrapolate the whole year from peak months), its PS is about 20-60x.

These numbers aren’t precise, nor do they need to be. We’re not filing with the SEC; we just want to judge if valuations are reasonable. And this hasn’t even touched the real issue.

The Real Issue: This Isn’t Recurring Revenue

These are not stable, enterprise-grade revenue streams. They are highly cyclical, speculative “repeat cash flows”:

-

Perpetual contract trading

-

Memecoin speculation

-

Fees from forced liquidations

-

MEV peak profits

-

Frequent inflows and outflows of high-risk speculative capital

In a bull market, fees and MEV soar; in a bear market, they disappear instantly.

This is not the recurring revenue of Software-as-a-Service (SaaS); this is Las Vegas-style casino revenue.

You wouldn’t give a “company that only makes money every 3-4 years when the casino is full” a Shopify-level valuation multiple. This is a different business model and deserves a different multiple.

Back to Fundamentals

By any reasonable logic: Ethereum, with a market cap of about $400 billion and annual (highly cyclical fee) revenue of only $1-2 billion, is not a value asset.

A 200-400x PS ratio, combined with slowing growth and value siphoned off by the Layer2 ecosystem, makes Ethereum less like a federal government in a tax system and more like a “federal government that can only collect state-level taxes while letting the states (L2s) take most of the revenue.”

We think of Ethereum as the “world computer,” but its cash flow performance is seriously out of sync with its market cap. Ethereum feels a lot like Cisco: an early leader with unreasonable multiples that may never reach its all-time high again.

In contrast, Solana’s relative valuation isn’t as crazy—not cheap, but not insane. With a $75-80 billion market cap and billions in annualized revenue, its PS is about 20-40x. Still high, still bubbly, but “relatively cheap” compared to Ethereum.

Let’s compare multiples: Nvidia, the world’s most sought-after growth stock, has a price-to-earnings ratio (note: P/E is one of the most commonly used stock valuation metrics, measuring stock price relative to company profitability. Formula: P/E = stock price / earnings per share) of only 40-45x, and it has:

-

Real revenue

-

Real profit margins

-

Global enterprise demand

-

Recurring contract-based sales

-

A huge customer base outside the crypto casino (fun fact: crypto miners were Nvidia’s first real hyper-growth driver)

Again: public chain revenue is cyclical “casino income,” not stable, predictable cash flow.

Logically, these public chains should have lower valuation multiples than tech companies, not higher.

If the industry’s fees can’t shift from “speculative capital churn” to “real, recurring economic value,” most assets will be repriced.

We’re Still Early... But Not That Kind of Early

Sooner or later, prices will realign with fundamentals, but that time hasn’t come yet.

The current reality is:

-

No fundamentals can support the high multiples of most tokens.

-

Once you strip out token inflation and airdrop arbitrage, many networks’ value capture will disappear.

-

Most “profits” are tied to speculative casino-like products.

We’ve built infrastructure for 24/7, low-cost, instant cross-border transfers... but made its best use case “slot machines.”

Short-term greed, long-term laziness. To quote Netflix co-founder Marc Randolph: “Culture isn’t what you say, it’s what you do.”

When your flagship product is “Fartcoin 10x leveraged perpetual contracts,” don’t talk to me about decentralization.

We can do better. This is the only way to upgrade from a hyper-financialized niche casino to a real, sustainable industry.

The End of the Beginning

I don’t think this is the end of crypto, but I do believe it’s the end of the beginning.

We’ve invested too much in infrastructure—over $100 billion sunk into public chains, cross-chain bridges, Layer2s, and all kinds of infrastructure projects—while seriously neglecting application deployment, product building, and real user acquisition.

We’re always bragging about:

-

Transactions per second (TPS)

-

Block space

-

Complex rollup architectures

But users don’t care about any of that. They only care about:

-

Is it cheaper?

-

Is it faster?

-

Is it more convenient?

-

Does it actually solve their problem?

Back to cash flow, back to unit economics, back to basics: Who are the users? What problem are we solving?

Where Is the Real Growth Potential?

For over a decade, I’ve been a steadfast crypto bull—that’s never changed.

I still believe:

-

Stablecoins will become the default payment channel.

-

Open, neutral infrastructure will underpin global finance behind the scenes.

-

Enterprises will adopt this technology because it makes economic sense, not for ideological reasons.

But I don’t think the biggest winners of the next decade will be today’s mainstream public chains or Layer2s.

History shows that every tech cycle’s winners emerge at the user aggregation layer, not the infrastructure layer.

The internet lowered computing and storage costs, but wealth ultimately flowed to Amazon, Google, Apple—companies that served billions of users by leveraging cheap infrastructure.

Crypto will follow a similar logic:

-

Block space will become a commodity

-

The marginal benefit of infrastructure upgrades will diminish

-

Users will always pay for convenience

-

User aggregators will capture most of the value

The biggest opportunity now is to integrate this technology into already scaled enterprises. Strip out pre-internet financial pipes, replace them with crypto infrastructure—if it truly lowers costs and increases efficiency, just as the internet quietly upgraded every industry from retail to manufacturing.

Enterprises adopted the internet and software because it made economic sense. Crypto is no different.

We can wait another decade for all this to happen naturally. Or, we can start now.

Update Our Understanding

So, where do we go from here? The technology works, the potential is huge, and we’re still in the early stages of real adoption.

It would be wise to reassess everything:

-

Evaluate network value based on real usage and fee quality, not ideology

-

Not all fees are equal: distinguish between recurring revenue and repeat cash flow

-

The winners of the last decade won’t dominate the next

-

Stop treating token price as a scoreboard for technological effectiveness

We’re still so early that we treat token price as the standard for whether the technology works. But no one chooses AWS over Azure just because Amazon or Microsoft stock went up that week.

We can wait another decade for enterprises to adopt this technology on their own. Or, we can start now and put real GDP on-chain.