Abnormal Aster trading volume? Unveiling the manipulation suspicions behind a 20x growth rate

Neither the user adoption curve nor the core mechanism upgrade can fully explain the rapid rise of Aster this time.

Neither the user adoption curve nor core mechanism upgrades can fully explain Aster's rapid rise this time.

Written by: DeFi Warhol

Translated by: Saoirse, Foresight News

Over the past week, I conducted an in-depth investigation into the surge in trading volume on the Aster platform and compared it with the Hyperliquid platform. The results clearly show that Aster's trading volume growth is not organic, but rather the result of artificially inflated trading volume, wash trading (creating fake trading activity through self-trading), and coordinated manipulation.

Below are my analytical arguments.

Why I Conducted This Investigation

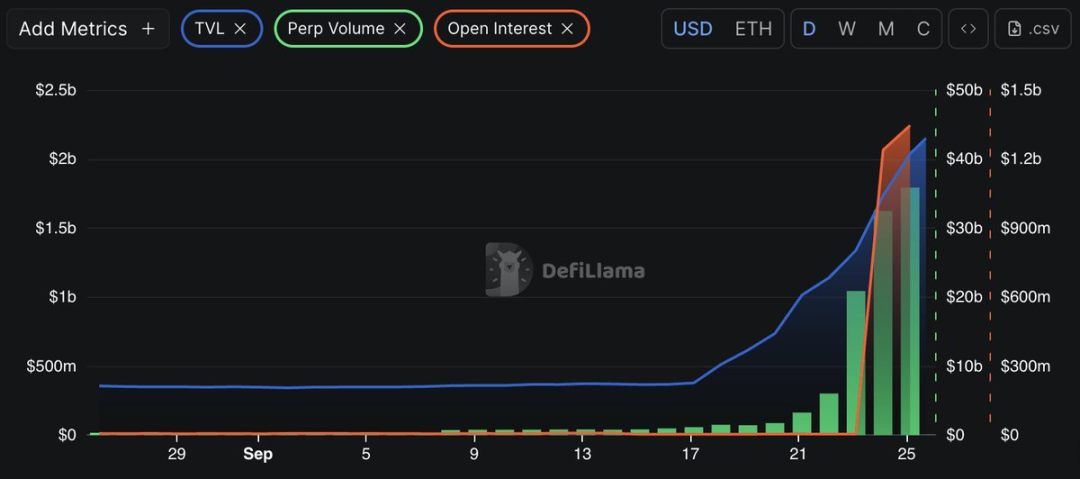

Within just 7 days from September 16 to 23, 2025, Aster's daily trading volume soared from $1 billion to $20 billion, which immediately aroused my suspicion. A 20-fold increase even surpasses the fastest growth rate of any compliant DeFi platform I have tracked.

At the same time, Aster's open interest (OI) surged about 33 times (from $3.7 million to $1.3 billion on September 24), and total value locked (TVL) jumped about 500% within 30 days. In contrast, Hyperliquid's metrics during the same period showed stable and organic growth.

The scale, timing, and speed of Aster's growth compelled me to investigate: are we witnessing a genuine explosive increase in platform users, or is this the result of artificial manipulation?

Abnormal Trading Volume

Data from Aster on September 17:

- Trading volume: $1.1 billion

- Total value locked (TVL): $378 million

- Open interest (OI): $3.62 million

Data from Aster on September 24:

- Trading volume: $32 billion

- Total value locked (TVL): $1.7 billion

- Open interest (OI): $1.2 billion

In contrast, Hyperliquid maintained a relatively stable trading volume pattern during the same period. The stability of Hyperliquid's trading volume highlights the artificial nature of Aster's trading volume surge.

Compliant trading volume growth usually follows a user adoption curve (i.e., a gradual increase in user numbers) and is associated with fundamental optimizations of the platform's underlying protocol. However, neither of these can fully explain Aster's rapid rise this time.

Large Transfers and Wash Trading Characteristics

- In the past 7 days, there were 156 large transfers over $10 million on the platform, with an average transfer size of $45.2 million, far exceeding typical DeFi trading levels.

- On September 25, FalconX completed 8 transfers totaling $680.4 million within 6 hours. Analysis of the transfer patterns shows coordinated operations between exchanges and unknown wallet addresses, with the timing perfectly matching the surge in Aster's trading volume.

- On September 24, within 3 hours, 7 consecutive USDT transfers from Binance to Aave were initiated, totaling $877.67 million. This series of transfers occurred just before the surge in Aster's trading volume. The timing correlation, combined with the systematic nature of the transfers, indicates organized liquidity manipulation aimed at artificially inflating trading metrics.

Fee and Revenue Structure

Data from DeFiLlama precisely confirms my suspicions:

- 24-hour fee revenue: $12.03 million

- 30-day fee revenue: $27.9 million

- Total value locked (TVL): $2.2 billion

Based on this, Aster's daily fee revenue to TVL ratio is about 0.55%, which is 14 times that of Hyperliquid (about 0.04%).

More importantly, only 59% of Aster's fee revenue can be converted into net income, while Hyperliquid's fee conversion efficiency is as high as about 99%. This difference indicates that most of Aster's fee revenue comes from artificial circular trading (i.e., generating fake fees through repeated buying and selling), rather than sustainable income from real traders.

Points System

In addition, Aster has launched a points system that awards points based on users' trading activity and volume.

The key issue with this system is that it directly incentivizes users to inflate trading volume:

- Wash traders can now not only earn fees through circular trading, but also gain points for rewards by inflating trading volume;

- This system essentially uses "user loyalty" as an excuse to legitimize circular trading (i.e., fake trades with no actual capital flow);

- The timing of the points system launch coincided with the peak of Aster's suspicious growth, indicating that the system was designed to perpetuate manipulation and provide a rationalization for it.

My Conclusion

Aster's growth is not organic, based on the following:

- Daily trading volume surged 20-fold in 7 days;

- Open interest soared 33-fold;

- Daily fee revenue reached $12 million, but net income conversion rate is extremely low;

- Highly dependent on Binance Smart Chain (BSC), with cross-chain wash trading cycles (i.e., generating trading volume through fake trades across different blockchain networks);

- The points system further amplifies the motivation for manipulation.

In summary, Aster's growth is an organized and coordinated manipulation, rather than genuine user recognition and business growth.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Analyst Sees Ethereum Potential Bottom Near $3,850 Amid Low RSI and Negative Funding

Bitwise Seeks SEC Approval for Innovative HYPE ETF

In Brief Bitwise filed for an ETF based on Hyperliquid's HYPE coin with the SEC. SEC delayed decisions on several other altcoin ETF applications. The cautious SEC approach fosters market uncertainty amid rising ETF applications.

Avalanche Climbs to $34.55 as Support Holds and Resistance Nears