The highly anticipated Plasma will go live tonight—can it change the landscape of on-chain payments?

Plasma positions itself as a settlement infrastructure for USDT and BTC, aiming to fill the gap left by Ethereum and Tron, and supports real-world payment flows.

Original Title: Plasma: The World of On-Chain Payments

Source: Sumcap

Translated by: Alex Liu, Foresight News

This article provides an in-depth analysis of Plasma, tracing the evolution of stablecoins and exploring how Plasma’s architecture is reshaping this sector.

From “Sound Money” to “Stable Money”

On January 3, 2009, the first bitcoin block was mined, embedding a message: “Chancellor on brink of second bailout for banks.” This referred to UK Chancellor Alistair Darling preparing to once again use taxpayer funds for a massive bailout of struggling banks—just months after the first rescue.

The first bitcoin block;

These bailouts occurred after the Wall Street crash in September 2008. When the 158-year-old investment bank Lehman Brothers filed for bankruptcy, its collapse sent shockwaves worldwide. Overnight, credit markets froze, and trillions of dollars in mortgage-backed securities became worthless—clearly demonstrating that “traditional finance” was untrustworthy: banks had taken reckless risks, regulators had turned a blind eye, and when everything collapsed, taxpayers bore the losses.

For many, BTC was seen as a direct byproduct of this crisis, standing in stark opposition to the existing banking system: i) fixed supply, ii) no central authority, iii) an inflation-resistant peer-to-peer network.

However, this “sound” money came with a trade-off: volatility when denominated in USD. As more people joined, the demand for predictable payments and invoicing grew. The alternative—(a) wiring funds to a bank, (b) waiting days for settlement, and (c) paying high fees in the process—only made things worse.

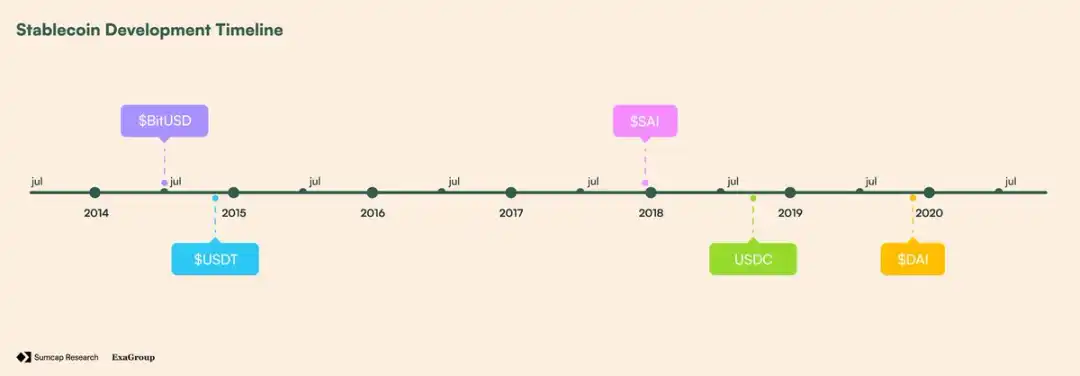

Eventually, in July 2014, BitShares launched BitUSD—allowing users to lock BTS (BitShares’ native token) as collateral and create a USD-pegged token. However, it was entirely dependent on BTS, meaning price drops could easily push collateralization below safe levels, triggering mass liquidations.

Just a few months later, in November 2014, Tether launched USDT—a fiat-backed token redeemable 1:1 for custodied dollars. Unlike BitUSD, it required no over-collateralization or complex mechanisms. This simplicity enabled it to reach $19.3 million in trading volume and a $1.45 million market cap in less than a year. For comparison, ETH was worth about $1 at the time, and BTC hovered around $240.

The success of USDT;

The success of USDT spawned more alternatives. MakerDAO (@SkyEcosystem) launched SAI in December 2017, allowing users to lock ETH into debt positions to mint a soft-pegged USD token, but ETH’s volatility forced an upgrade: in November 2019, Multi-Collateral Dai (DAI) was launched. By diversifying collateral and adding risk controls governed by MKR, DAI became the first truly adopted decentralized stablecoin.

Meanwhile, fiat-backed competitors developed in parallel: USDC launched in 2018, positioning itself as a regulated, fully dollar-backed token with transparency certification, quickly becoming DeFi’s preferred collateral.

Stablecoin development timeline

Stablecoin Adoption and Infrastructure Gap

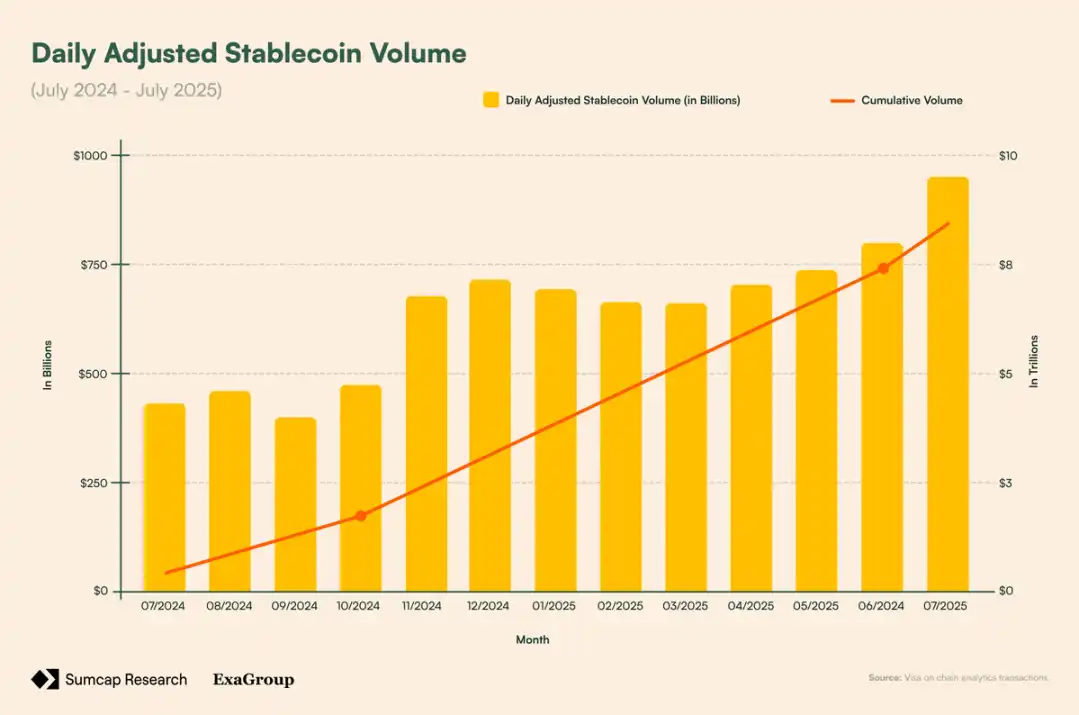

Today, by trading volume, stablecoins are the most widely used product in crypto. Their market cap ($271.6 billion) now exceeds DeFi’s total value locked ($166.1 billion). In 2024, while Visa processed $13.2 trillion in payments, stablecoins settled over $22 trillion in raw on-chain volume—after adjusting for exchange internal transfers and MEV, that’s $5.67 trillion. Additionally, adjusted daily trading volume grew about 120% year-on-year (from $432.3 billion to $949.1 billion), highlighting rising demand.

Adjusted stablecoin daily trading volume;

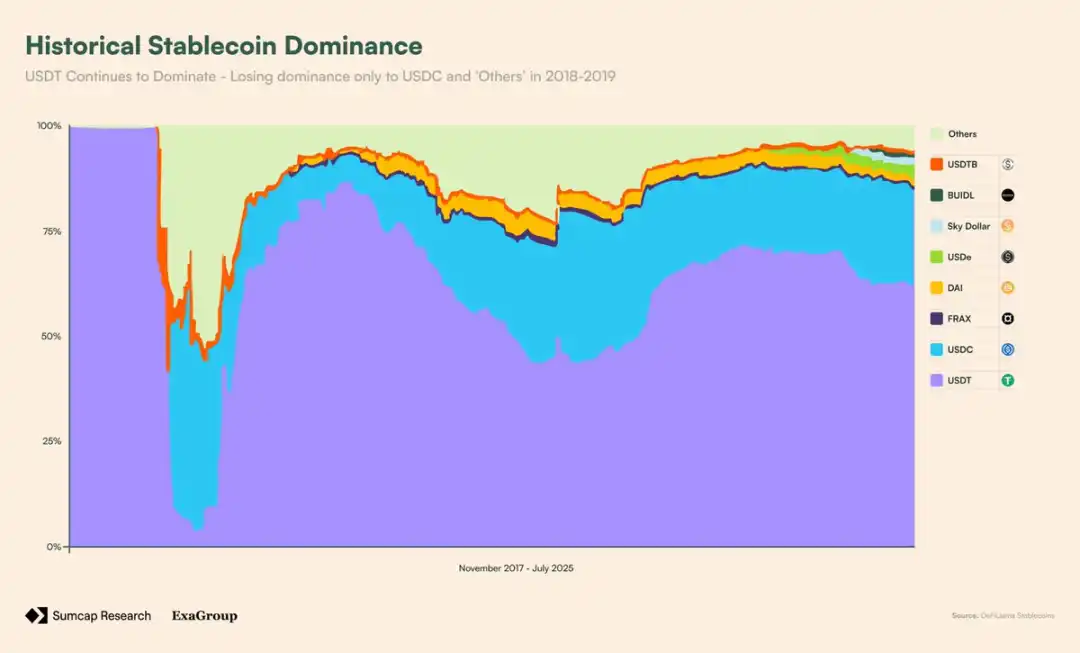

In July 2025, the US “Genius Act” officially recognized stablecoins as legal payment instruments, putting them on par with debit card networks, ACH, and wire transfers. Nevertheless, infrastructure still lags behind. USDT, with over 60% market share, still relies on general-purpose chains not designed for payments, where transfers require volatile gas tokens, and institutional scalability and compliance needs remain unmet.

USDT’s dominance;

This creates a paradox: stablecoins’ annual transaction volume rivals Visa, but on-chain they remain second-class citizens, treated as just another token.

Bitcoin faces a similar issue. As the world’s seventh-largest asset and with a market cap higher than silver, BTC should be DeFi’s anchor. Yet, most of it sits idle. Wrapped BTC solutions are fragmented and custodial, with independent versions on Ethereum, Polygon, and Arbitrum—each with siloed liquidity.

Plasma Architecture: A Stablecoin-First, Natively BTC-Supported Blockchain

To solve this, Plasma rethinks the foundation itself. Rather than treating stablecoins and BTC as add-ons, it makes them first-class citizens through purpose-built components:

· PlasmaBFT - A pipelined version of Fast-HotStuff, offering fast finality without sacrificing security

· Reth Execution Layer - An EVM-compatible execution engine written in Rust

· Native BTC Bridge - A decentralized validator network securing pBTC operations

· Stablecoin-centric features - Native gas paid in USD, zero-fee transfers via paymaster, and auditable confidential payments.

With this architecture, Plasma diverges from general-purpose design, aiming to be the natural settlement layer for BTC-USDT activity.

PlasmaBFT

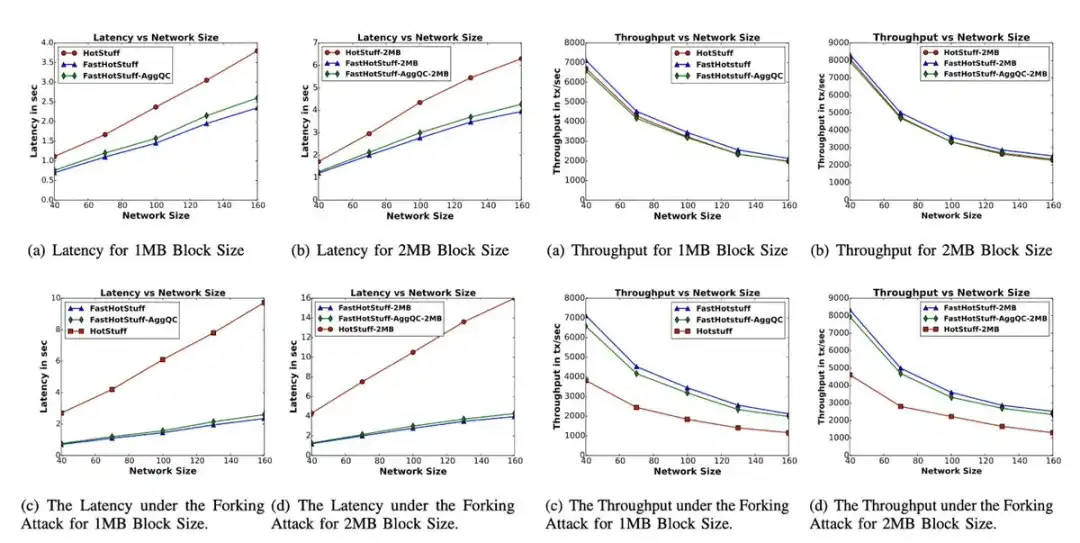

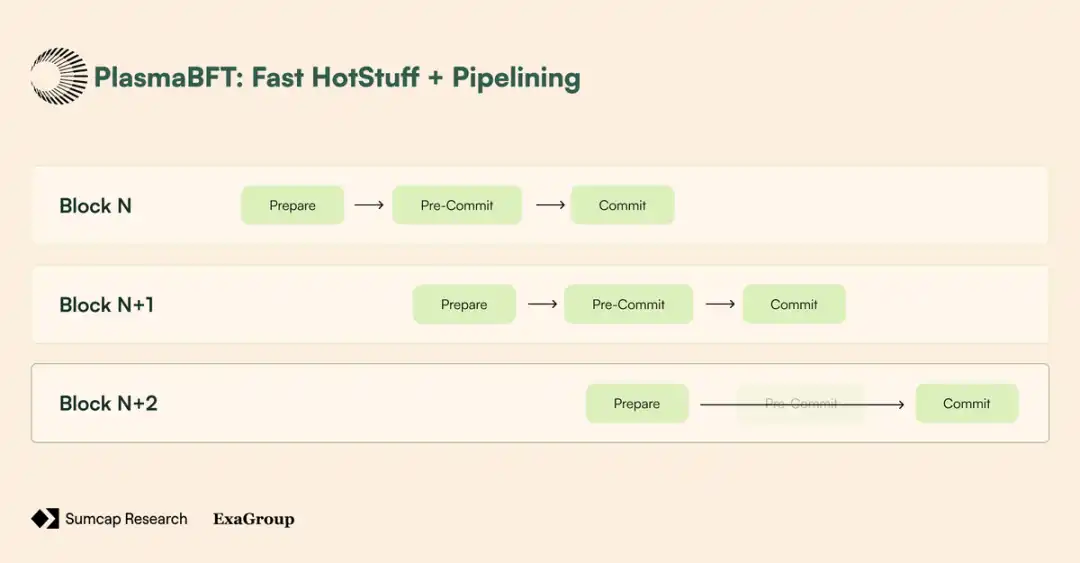

Plasma’s consensus layer secures the chain with a high-performance implementation of Fast-HotStuff. In traditional BFT protocols like HotStuff, finalizing a block requires three phases:

· Prepare – The leader proposes a block, validators check its validity and vote to approve;

· Pre-commit – Validators confirm a supermajority (>⅔) approved the prepare phase, then “lock” on the block to prevent forks;

· Commit – Validators confirm a supermajority pre-committed, making the block finalized and irreversible.

While this process ensures security, it slows things down, as each step requires network communication and coordination. Fast-HotStuff reduces this overhead with the so-called “two-chain commit rule”: if two consecutive blocks (N and N+1) both receive supermajority approval, N can be finalized immediately, since the supermajority on N+1 proves validators were locked on N when approving N+1—thus, no pre-commit phase is needed.

In practice, the three phases are simplified to two:

· Phase 1 (Prepare) – Vote on block N

· Phase 2 (Commit) – Vote on block N+1, thereby finalizing block N

FHS vs HS comparison;

Moreover, in cases where the network can’t achieve two consecutive supermajorities for fast finality, PlasmaBFT falls back to the full three-phase commit protocol, ensuring all honest validators are safely “locked” on the same block before finalization. Once the fallback is resolved, PlasmaBFT resumes the fast two-phase path.

FHS vs HS workflow comparison

But that’s not all. With pipelining, multiple block phases can overlap and be processed simultaneously: while validators are in the commit phase for block N, they may already be in the prepare phase for block N+1. This keeps the network busy at all times, maximizing efficiency, as the next block’s voting can start before the previous one is fully finalized.

Additionally, by selecting only a subset of validators (a committee), PlasmaBFT reduces communication overhead while still applying the same supermajority rules.

FHS + pipelining

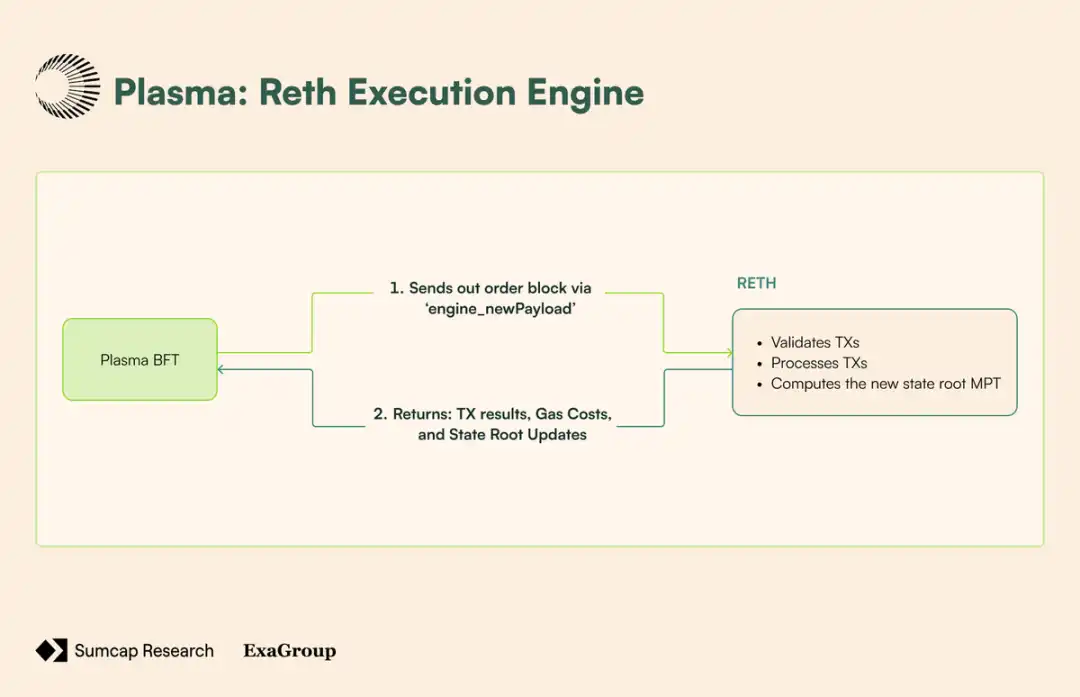

Reth Execution Engine

Plasma’s execution layer is built on Reth, an Ethereum client written in Rust, fully compatible for managing state transitions, transaction processing, and EVM operations. It connects to the consensus layer via the same engine API Ethereum has used since “the Merge”—allowing PlasmaBFT to handle consensus and block ordering, while Reth focuses on transaction execution and state transitions:

1. Block proposal – The CL sends ordered blocks to Reth via engine_newPayload call

2. Transaction validation – Reth verifies each transaction’s format, signature, nonce, and gas requirements

3. State execution – Reth processes transactions in order

4. State root calculation – After all transactions are executed, Reth uses a Merkle-Patricia tree to compute the new state root and transaction receipt root

5. Execution confirmation – Reth returns the execution results (including gas usage, transaction receipts, and updated state root) to PlasmaBFT

6. Block finalization – PlasmaBFT incorporates the execution results into the final block header and completes the consensus process

RETH workflow

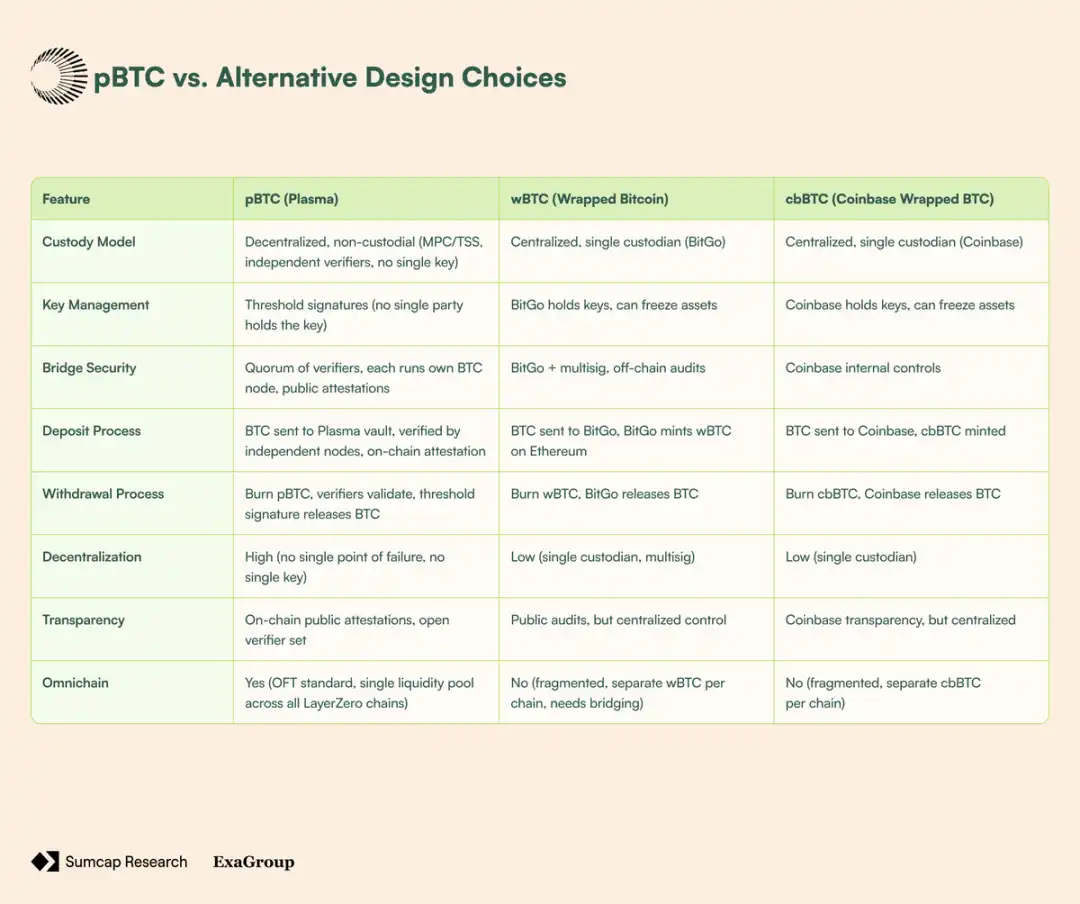

Native BTC Bridge

Most BTC bridges today appear decentralized on the surface, but peel back the layers and you’ll find either:

· A single custodian (like wBTC’s issuer BitGo) holding everyone’s coins, or

· A small multisig wallet that can freeze the treasury at any time.

This is the trade-off users have accepted: if you want to use BTC in DeFi, you must give up bitcoin’s trust-minimized design.

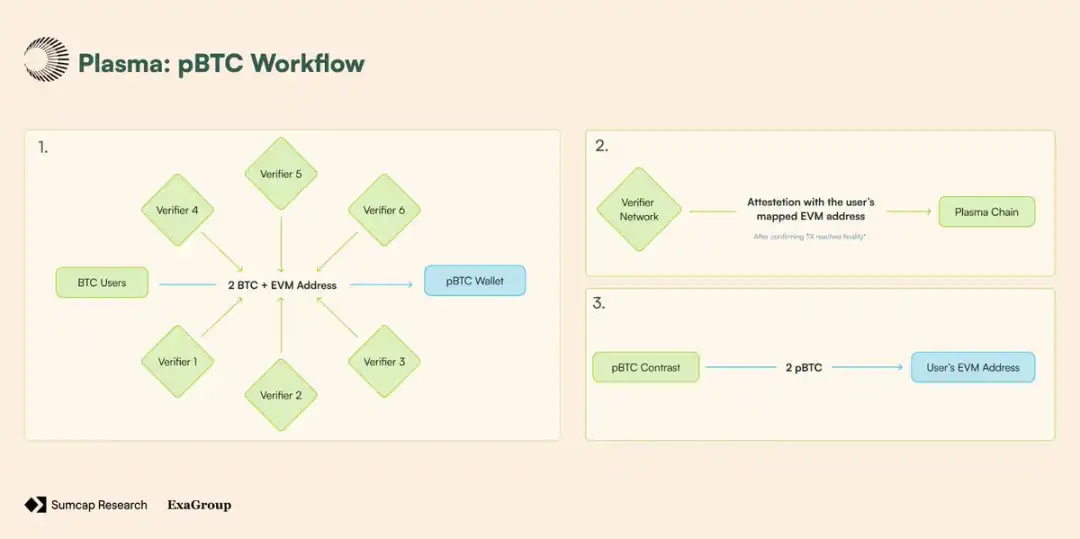

Plasma’s BTC bridge is not custodian-driven, but powered by a validator network, each running its own bitcoin node. No single party controls the treasury; BTC deposits and withdrawals must be collectively approved by a threshold signature from a quorum of validators.

When a user deposits BTC into a Plasma vault on the bitcoin network, each validator: independently “sees” the deposit via its own bitcoin node, confirms the deposit is finalized, and then broadcasts a proof on-chain.

These public proofs confirm BTC has been received and carry the user-mapped EVM address. Once a supermajority of validators agree, pBTC is minted directly to the user’s address on Plasma, and the proof is sent on-chain.

Figure 10 – pBTC workflow;

But improved trust model is only part of the story. Most BTC bridges today also suffer from another key flaw: liquidity fragmentation. Take wBTC as an example—it exists as a separate version on each chain. wBTC on Ethereum cannot interact directly with wBTC on Polygon or Arbitrum, except through extra cross-chain steps and independent liquidity pools, adding complexity for users and protocols.

Plasma solves this by implementing pBTC using LayerZero’s OFT (Omnichain Fungible Token) standard, creating a single token across all LayerZero-connected chains. This creates a unified liquidity pool for pBTC spanning the entire omnichain ecosystem.

pBTC vs alternative design choices;

Stablecoin Native Design

· Zero-fee USDT transfers: Contract-level paymaster sponsors the transfer and transferFrom functions via an account abstraction system built on EIP-4337 and EIP-7702 standards.

· Custom gas token: Protocol-managed paymaster uses EIP-4337 standard, calculates gas costs based on oracle-provided rates (with slippage protection), and charges no fees.

· Confidential payments: Hides amounts, recipients, and metadata, while retaining selective disclosure for compliance.

Competitive Landscape and Opportunity Size

Total Addressable Market

We’ve all heard the classic business analogy: “Better to be the head of a chicken than the tail of a phoenix.”

Plasma embodies this in the world of on-chain payments and yield market opportunities. Plasma does not compete as another general-purpose chain with technical innovations of little practical benefit, but laser-focuses on becoming infrastructure for institutional use.

“Native BTC”: Tokenization and Yield Market Opportunity

Despite being the largest crypto asset, BTC is mostly unused in DeFi—wrapped products strip away all its trust-minimized ethos.

BTC in wrapping;

As the most decentralized BTC wrapping solution, pBTC offers “native BTC” DeFi opportunities that others cannot replicate. Currently, over 242,600 BTC are wrapped, of which 209,800 BTC (about 86.5%) are actually deployed in various protocols to earn yield—the core opportunity for pBTC comes from retail users seeking a safer way to:

· Use BTC in DeFi;

· Store BTC on more accessible EVM chains.

But retail demand is only part of the story. Institutional and corporate adoption is rising, with public and private companies now holding about 1.38 million BTC. This is up 833,000 BTC since the start of the year—highlighting a clear trend of accelerating institutional adoption.

BTC held by institutions and companies;

But here’s a key insight: as more institutions add BTC to their treasuries, their strategies will evolve from simple holding to active management. For this, pBTC represents the perfect intermediary—since these participants put infrastructure security above all else.

On-Chain Payments: Cross-Border Remittances and Payroll

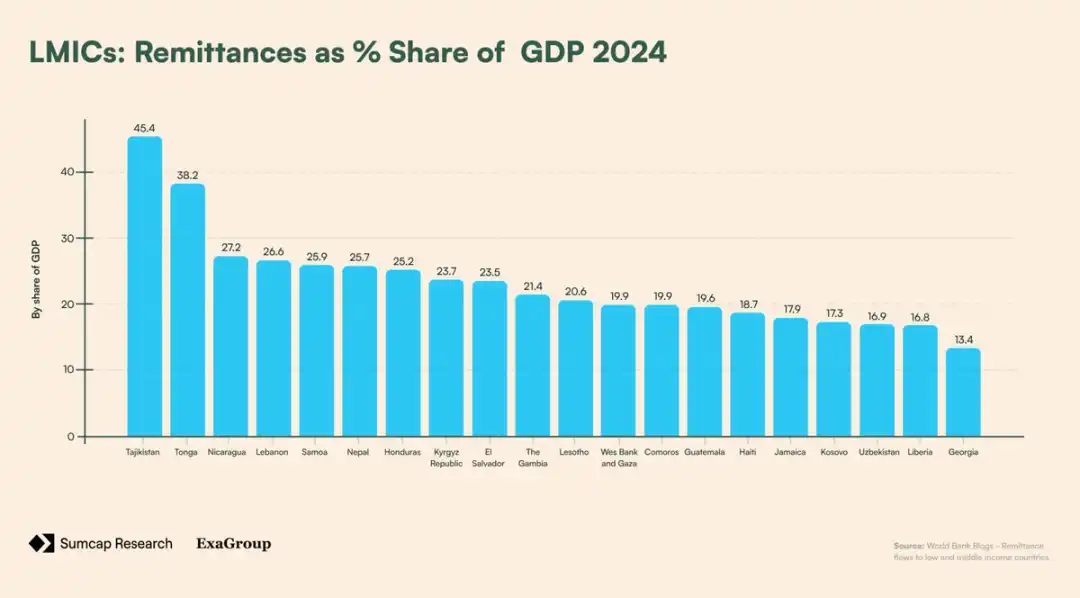

In 2023, it was reported that 184 million people (2.3% of the world’s population) lived outside their country of nationality. Driven by economic opportunity, these migrant workers often need to send money home across borders. These cross-border payments (or “remittances”) play a crucial role in supporting the economies of low- and middle-income countries—accounting for up to half of GDP in some cases.

LMICs by remittance as % of GDP;

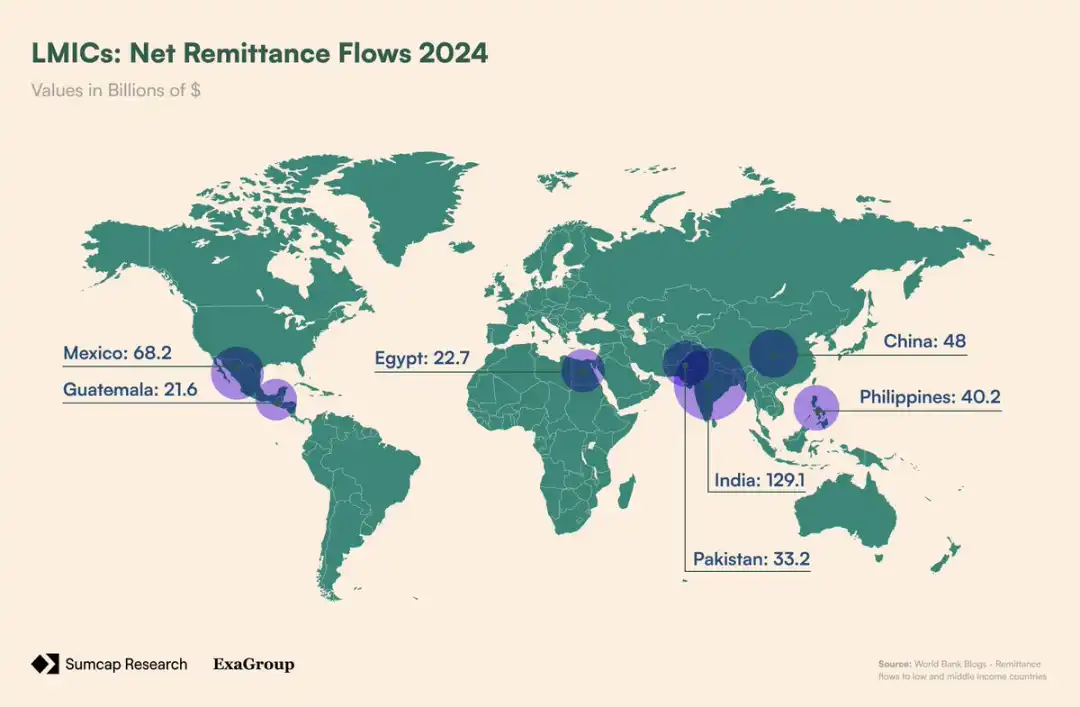

In 2024, remittances to low- and middle-income countries reached $685 billion, with the top five recipients being:

1. India – $129 billion

2. Mexico – $68 billion

3. China – $48 billion

4. Philippines – $40 billion

5. Pakistan – $33 billion

LMICs net remittance inflows;

These massive flows are a lifeline for millions of families worldwide—but they come with hidden costs. Take India as an example. In 2023, India reportedly received $16 billion in remittances from the US. At an average transfer cost of 4.16% per $200 (exchange rate margin + fees), $66.5 million was siphoned off by banks/forex agencies. This pattern repeats in every major remittance corridor. Mexico receives over $50 billion annually from the US, losing over $2.4 billion to fees at current transfer costs. Meanwhile, Nigeria receives $6 billion from the US, losing $180 million.

Plasma’s opportunity here is clear. With zero-fee USDT transfers, Plasma can eliminate the billions of dollars extracted annually from vulnerable populations by traditional channels. Migrant workers can finally send the full $200 to their families in Guatemala, instead of $187 after fees. Over time, this will save each family thousands of dollars—money that stays in the communities that need it most.

However, remittances are only part of Plasma’s reach. Combining zero-fee USDT transfers with auditable confidentiality, Plasma opens a whole new market: on-chain payroll.

In 2023, the US alone generated $11.07 trillion in wages and salaries, involving 134.06 million employees. That’s 1.6 billion (12 × 134 million) bank transfers per year—all incurring costs for companies.

For simplicity, assume these wages are paid monthly via ACH direct deposit. With a fixed fee per transfer ranging from $0.20 to $1.50, US companies spend about $1.37 billion annually just to move money into employees’ accounts:

134.06 million × 12 × $0.85 = $1.37 billion

As with remittances, funds that could be better used by companies making the transfers are wasted on fees. By adopting Plasma’s gasless USDT transfers, US employers would save about $1.4 billion annually, while confidentiality adds another layer of value for both employers and employees.

Opportunity Size Assessment

Plasma sits at the intersection of the world’s three largest capital flows:

1. Savings and capital allocation—enabling users to earn yield on BTC in DeFi.

2. Cross-border payments—saving billions in remittance fees.

3. Payroll—eliminating friction and fees in domestic and international wage payments.

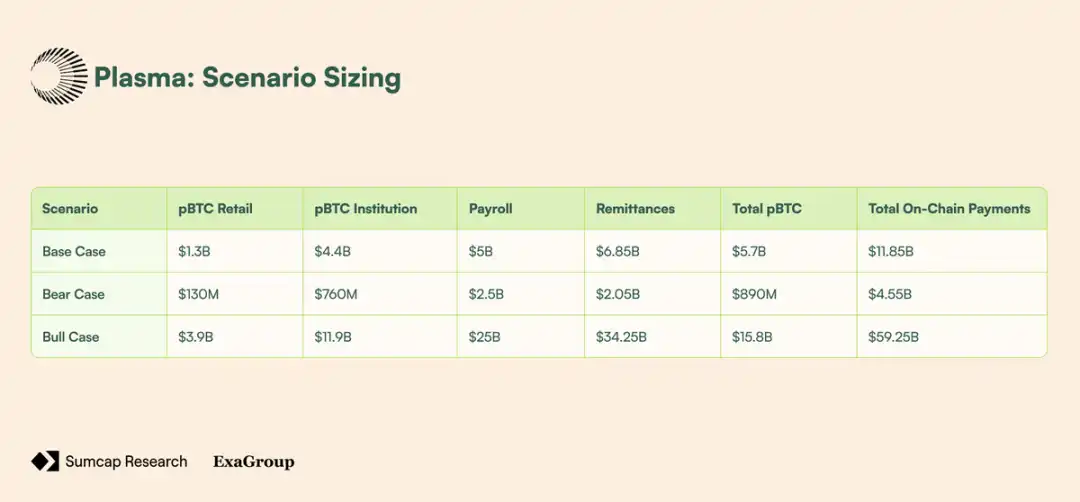

Even modest adoption in each of these areas is enough to support a multi-billion dollar TAM. Assessing these opportunities under different adoption scenarios yields three cases: base, pessimistic, and optimistic.

Base case: pBTC adoption comes from retail users seeking safer alternatives and early institutional interest in DeFi yield. On-chain payments grow as remittance cost savings gain attention and a small wave of tech companies experiment with crypto payroll.

Pessimistic case: Wrapped BTC remains dominant due to familiarity and integration, leading to lagging adoption. Regulatory uncertainty and crypto knowledge gaps slow institutional inflows and remittance usage, while payroll faces resistance from existing systems.

Optimistic case: Improved user experience, regulatory clarity, and mainstream adoption drive mass BTC migration, remittance flows, and enterprise payroll integration.

Scale assessment for each scenario;

Competitive Landscape

Plasma’s competitive landscape is as follows:

· TronDAO – Dominates USDT circulation, but limited by centralization, scalability constraints, and rising costs.

· Ethereum – The base for issuance and large transfers, but high fees, delays, and block space competition make it unsuitable for retail payments.

· USDC – Positioned as a regulated, transparent option, but its usage skews toward financial platforms and exchanges, with little representation in real-world commerce.

Competitive landscape

Conclusion

The evolution of crypto payment infrastructure has been shaped by incremental workarounds, not deliberate design. This has led to a mismatch between the assets driving adoption (BTC and USDT) and the infrastructure they rely on.

Plasma addresses these inefficiencies by re-architecting the foundation around these assets:

· Making stablecoins the native gas asset, eliminating reliance on volatile tokens and enabling payroll and remittances.

· pBTC integrates cross-chain liquidity via LayerZero’s OFT standard and enables productive BTC deployment in DeFi.

· Privacy and compliance features align with enterprise needs for predictable costs and operational security.

Its impact spans multiple market segments:

· Enterprises gain cost-predictable, compliant settlement methods.

· Institutions can productively deploy their BTC treasuries.

· Retail users unlock instant, low-cost remittance and payroll receipt.

Plasma positions itself not as a general-purpose chain, but as settlement infrastructure purpose-built for USDT and BTC. By aligning infrastructure with the most important assets, it fills the gaps left by Ethereum and Tron, supports real-world payment flows, and opens the next era of adoption across retail, enterprise, and institutional layers.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why Eastern Europe Is Becoming the Next Crypto Hub

[Long English Thread] In-Depth Analysis: How Can Plasma Change the Landscape of On-Chain Payments?

Retail Traders Chase the Next Big Crypto to Hit $1 as BTC Consolidates Under Heavy ETF-Driven Resistance

Australia Plans 10% Revenue Fines for Crypto Firms