Speculation on the New Fed Chair: How Would Waller Influence the Crypto Wallet?

Written by: David, TechFlow, Deep Tide

Original Title: US Stocks & Crypto's Purse Strings—He Might Decide Their Future

There are still 9 months left in Powell's term, but discussions about who will succeed as Federal Reserve Chair have already reached a fever pitch.

The Chair of the Federal Reserve may be the most powerful economic position in the world. A single word from him can cause violent swings in capital markets, and one decision can influence the flow of trillions of dollars. Your mortgage rate, stock market returns, and even the volatility of crypto assets are all closely tied to decisions made in this position.

So who is most likely to be the next Chair? The market is gradually giving its own answer.

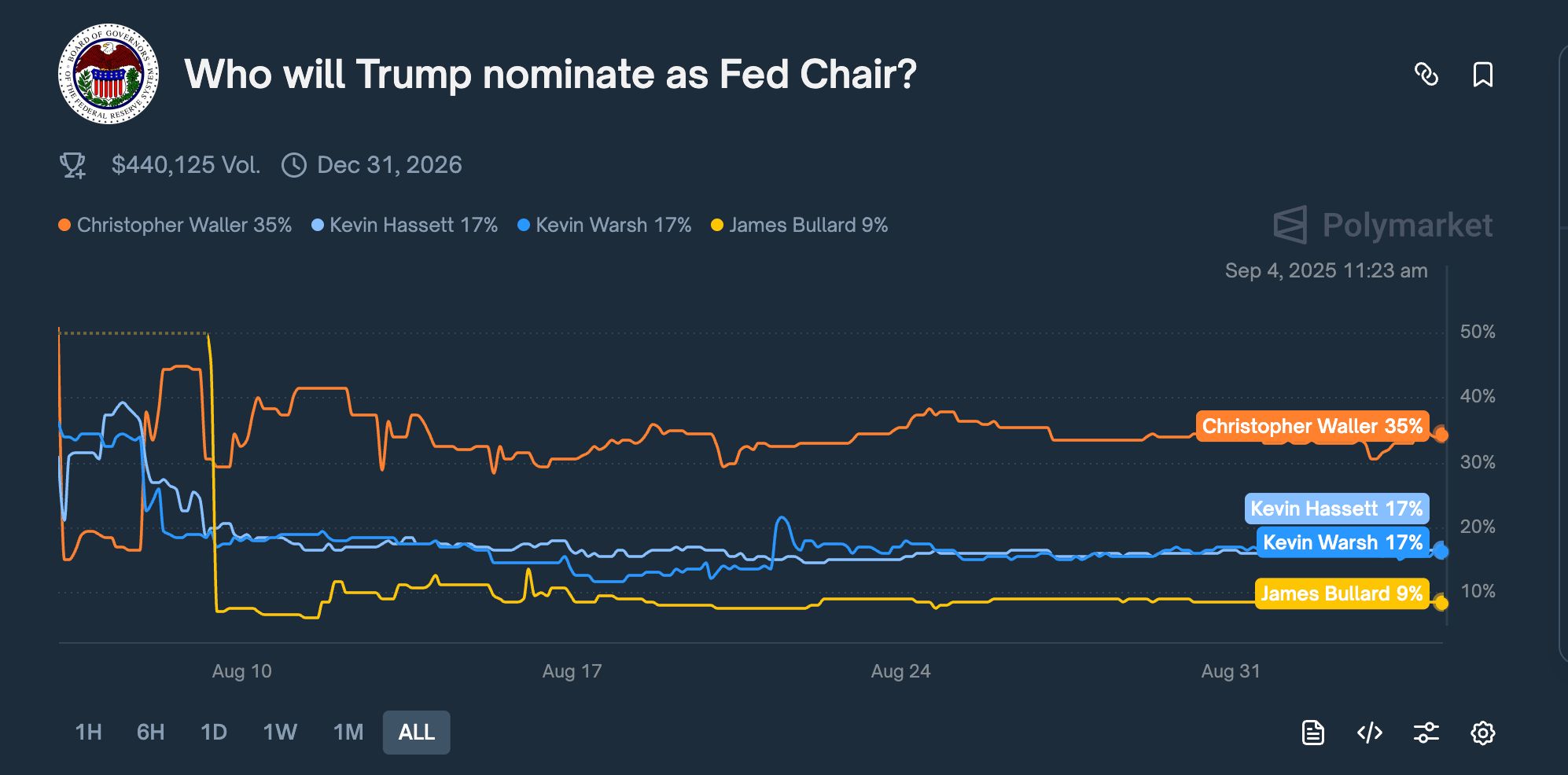

On August 7, on the prediction market Kalshi, Federal Reserve Governor Christopher Waller's odds surged from 16% the previous day to over 50%, surpassing all other competitors for the first time. Although the odds fluctuated afterward, Waller has consistently maintained the lead.

According to the latest data, Polymarket shows Waller still leading with a 35% probability, ahead of other popular contenders Kevin Hassett and Kevin Warsh, both at 17%.

Why has the market suddenly become bullish on this 65-year-old current Fed Governor?

A recent Bloomberg report may provide a clue: Trump's advisory team believes Waller is "willing to make policy based on forecasts rather than current data" and "has a deep understanding of the Federal Reserve system."

More importantly, Waller was nominated to the Fed by Trump in 2020. And at the July 30 FOMC meeting, Waller himself did something particularly eye-catching:

He, along with fellow Governor Michelle Bowman, cast a dissenting vote, arguing that the Fed should cut rates by 25 basis points. This was the first time since 1993 that two governors simultaneously opposed a decision to keep rates unchanged.

What Trump needs now is a Fed Chair who can both push for rate cuts and not be seen by the market as a White House puppet; from this perspective, Waller seems to fit the bill perfectly.

Political Acumen: Choosing the Right Moment to Take a Stand

To understand Waller, we must start with this dissenting vote.

First, some background: The Federal Reserve's Federal Open Market Committee (FOMC) meets eight times a year to decide the US benchmark interest rate. This rate is the main valve of the US economy, determining the cost of borrowing between banks and, in turn, affecting all loan rates.

Participants must collectively vote on rate changes. For decades, these votes have been almost unanimously passed. In Fed culture, publicly casting a dissenting vote is seen as a challenge to the Chair's authority.

The July 30, 2025 FOMC meeting was particularly sensitive.

The Fed had kept rates unchanged at 4.25%-4.5% for five consecutive times. Meanwhile, Trump was attacking Powell daily on Truth Social, calling him "too late" and "stupid," demanding immediate rate cuts to stimulate the economy.

Just two weeks before this meeting, on July 17, Waller gave a sharp speech at the New York University Money Marketeers Association:

"I always tell my new colleagues, speeches are not murder mysteries—just tell the audience who did it, just tell them the point."

The point of this speech, naturally, was his belief that the FOMC should cut rates by 25 basis points; and the "culprit" was projected onto the Fed itself.

Publicly taking a stance is generally not in line with central bank officials' codes of conduct. But perhaps this was a carefully chosen moment by Waller for political maneuvering.

By expressing his views in advance, it made the dissenting vote at the FOMC formal meeting two weeks later appear to be a result of long-term professional judgment, rather than succumbing to political pressure.

On July 30, when Waller and Bowman voted against keeping rates unchanged, it was indeed the first time since 1993 that two governors had simultaneously dissented, which naturally drew attention.

The market interpreted this as a sign of rational dissent within the Fed; but from Trump's team's perspective, it looked more like Waller taking a stand and picking a side.

Even more cleverly, Waller also voiced his opinion on current tariff policy: "Tariffs are a one-time increase in price levels and will not cause sustained inflation." This statement became his signature argument quoted by various media outlets.

To translate, the subtext is:

Trump's tariffs do indeed push up prices, but only temporarily. So rate cuts shouldn't be withheld just because of tariffs. Clearly, Waller's view neither criticizes Trump's tariff policy nor provides an economic rationale for rate cuts.

Using an economic theory to resolve a political dilemma; choosing the right moment to express a rate-cut stance aligned with the President.

Betting Against Former Treasury Secretary, Predicting a Soft Landing

If casting a dissenting vote showcased Waller's political acumen, then correctly predicting the economic trajectory demonstrated his solid professional skills.

First, some background.

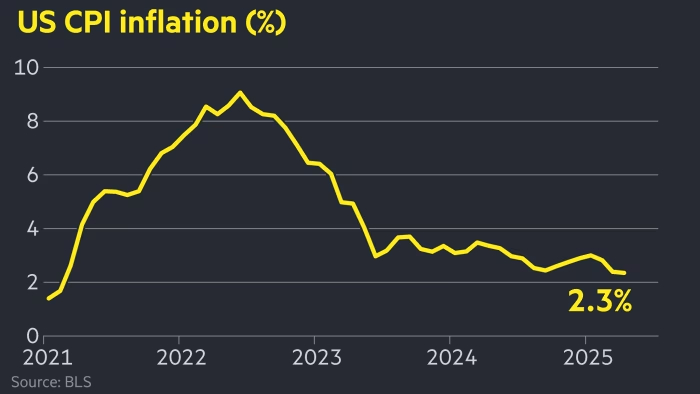

In June 2022, US inflation hit 9.1%, a 40-year high. What does this mean?

If you deposited $10,000 at the beginning of the year, by the end of the year your purchasing power would be only $9,000. Gas prices doubled, and eggs rose from $2 to $5.

The Fed faced a tough choice. To lower inflation, it had to raise rates. Higher rates make loans more expensive, discouraging businesses from borrowing to expand and consumers from taking out loans for homes or cars, cooling the economy and reducing inflation.

But the problem is, too strong a dose can cause trouble. Historically, every time the Fed has raised rates sharply, it has triggered a recession.

At this point, a rare public debate broke out among economists.

On one side were three heavyweight economists: former Clinton Treasury Secretary Summers, former IMF Chief Economist Blanchard, and Harvard economist Domash.

In July, they published research arguing that the Fed could not control inflation without causing a "painful" spike in unemployment. To bring inflation down, unemployment must rise. This is an economic law, like a law of physics.

Summers' team's calculation was that to bring inflation down from 9% to 2%, unemployment would have to rise to at least 6%. That would mean millions losing their jobs.

But Waller disagreed.

On July 29, he and Fed economist Andrew Figura published a paper, "How Likely Is a Soft Landing? What Does the Beveridge Curve Tell Us?" directly challenging Summers' team's conclusions.

Waller's core argument was that this time was different, because the pandemic had caused unprecedented distortions in the labor market.

Many people retired early, and many were unwilling to work due to the pandemic. This led to artificially high job vacancies; it wasn't that the economy was so hot that everyone was hiring, but that fewer people were willing to work.

The paper concluded: a soft landing is a "reasonable outcome," and the US could bring inflation back to normal with only a slight rise in unemployment.

On August 1, Summers and Blanchard quickly fired back, saying Waller's paper "contains misleading conclusions, errors, and factual mistakes."

Central bank officials usually speak cautiously, and scholars are usually polite. But this time, both sides spoke strongly, as if defending the correctness of their economic theories.

The market naturally sided with Summers. After all, he was a former Treasury Secretary, Blanchard a former IMF Chief Economist. Waller was "just" a Fed Governor.

The next 18 months became a public test and wager.

By the end of 2022, commodity prices began to fall. In early 2023, supply chain pressures eased. The Fed did indeed raise rates sharply, from near 0% all the way up to 5.5%.

Everyone was waiting to see if a wave of unemployment would come, but the result was surprising.

By the end of 2024, inflation had dropped below 3%, while unemployment was only 3.9%. There was no recession, nor mass layoffs.

In September 2024, Waller and Figura updated their research paper, even adding an "s" to the title—from "Soft Landing" to "Soft Landings," implying this was not a fluke, but repeatable.

Waller won this bet.

This academic showdown also proved Waller's ability to challenge authority and make independent judgments; for Trump's team, this was even more valuable. They saw someone willing to challenge the mainstream and who believed in the resilience of the US economy.

Midwestern Scholar, Braving Washington

Waller, unlike most people who serve at the Fed, has a unique career path.

Born in 1959 in Nebraska City, Nebraska, a small town of only 7,000 people, Waller spent his childhood in South Dakota and Minnesota—Midwestern agricultural states far from the East Coast's financial centers.

Seats on the Fed Board are usually occupied by a certain type of person: Ivy League graduates, Wall Street veterans, or those who have worked in Washington government departments. They often speak the same language and share similar worldviews.

Waller clearly does not belong to that group.

Waller started at Bemidji State University, where he earned a bachelor's degree in economics; you may never have heard of this place in northern Minnesota, where winter temperatures can reach minus 30 degrees.

Such an upbringing may make it easier to see the real America, and those ordinary people living in small towns, taking out loans to buy homes and cars, worrying about jobs and prices.

In 1985, Waller earned a PhD in economics from Washington State University and began a long academic career.

First at Indiana University, then the University of Kentucky, and finally at Notre Dame; for 24 years, he taught and did research. Waller's research focused on monetary theory, one of the most abstract branches of economics.

This kind of research clearly won't get you on TV or make you a celebrity economist, but it might come in handy at critical moments. In 1996, Waller co-authored a paper, "Central Bank Independence, Economic Behavior, and Optimal Term Length."

This paper studied a practical and timely question: How long should a central bank governor's term be?

The core finding was: if the term is too short (e.g., 2 years), the governor will yield to political pressure because he wants to be reappointed. If the term is too long (e.g., 14 years), he may become detached from reality and inflexible.

Twenty-five years later, this theoretical paper became a practical guide.

In 2020, when Trump publicly criticized the Fed and demanded rate cuts, the newly appointed Waller faced a choice: fully comply, or fully resist?

He chose a third path: support rate cuts at certain times, such as casting a dissenting vote in July 2025; but the reasons must be professional, not simply because the President wants rate cuts.

This delicate sense of balance—neither so independent as to ignore political reality, nor so dependent as to lose professional judgment—was exactly what he had studied more than 20 years ago.

In other words, Waller's navigation of the Fed is not just a matter of intuition, but is based on a set of academically validated balancing theories.

Before joining the Fed, Waller also "leveled up" in the "training ground."

The Fed is not a single institution, but consists of the Washington Board and 12 regional Feds. Each regional Fed has its own research department and policy leanings.

In 2009, at age 50, Waller left academia to join the St. Louis Fed as Director of Research, a position he held for 11 years. Waller managed a research department of over 100 people, with daily work including economic data analysis, policy report writing, and FOMC meeting preparation.

What truly changed his career trajectory was being nominated to the Fed Board by Trump in 2019.

This nomination was itself controversial. Waller's confirmation process was not smooth; Democratic senators questioned his independence, since he was a Trump nominee. Republican senators worried he was too academic and not "loyal" enough.

On December 3, 2020, the Senate narrowly approved his appointment by a 48:47 vote, one of the closest results in recent years. At 61, Waller joined the Fed's top decision-making body, older than most governors. But this became an advantage.

The typical Fed governor's path is predictable: elite school → Wall Street/government → Fed. They enter the power center in their 40s, with enough time to build networks and learn the rules of the game.

Waller is different. He spent 24 years in academia, 11 years at a regional Fed, and only came to Washington at 61.

Compared to other governors, Waller has less baggage and owes no favors to Wall Street; having worked at the St. Louis Fed, he knows the Fed is not monolithic—different voices are not only tolerated, but sometimes encouraged.

When Trump's team evaluates who can succeed Powell, these may be exactly the qualities they see:

Someone old enough, with nothing left to prove; someone with independent judgment, but who knows how to express it within the system.

Bullish for Crypto?

If Waller really becomes Fed Chair, what benefits might it bring?

The market's first reaction is that Waller will cut rates. After all, he cast a dissenting vote in July supporting a rate cut. Trump has also consistently demanded lower rates.

But a closer look at his record shows things are more complex.

In 2019, when the economy was strong, Waller supported rate cuts. In 2022, when inflation soared, he supported aggressive rate hikes. In 2025, he turned back to supporting rate cuts…

His principle seems clear: loosen when needed, tighten when needed. If he becomes Chair, rate policy may become more "flexible," not mechanically following Trump's rules, but adjusting quickly according to economic conditions.

But Waller's real difference may not lie in traditional monetary policy, but in how he views new things like crypto and stablecoins.

On August 20, when asked how the Fed should respond to financial innovation, Waller said there was "absolutely no need to worry about digital asset innovation"; at a stablecoin conference in California this February, he said stablecoins are "digital assets designed to maintain stable value relative to national currencies."

Note, he emphasized the relationship with national currencies, not something independent of the monetary system. This difference in perspective could lead to a fundamental policy shift.

Currently, the US attitude toward digital assets is defensive—concerned about money laundering, financial stability, and investor protection; the focus of regulation is "risk control."

Waller clearly opposes central bank digital currencies, arguing that "it's unclear what market failure in the US payment system it would solve," but he supports another path: allowing private stablecoins to innovate and take on the functions of a digital dollar.

But all these ideas are premised on Waller being able to withstand pressure.

He has not experienced a true financial crisis. In 2008, when Lehman collapsed, he was teaching. In 2022, when FTX went bankrupt, he had just joined the Fed and was not yet a core decision-maker.

Moving from governor to Chair is not just a change in position. Governors can express personal views; every word from the Chair can shake the market.

When the stability of the entire financial system rests on your shoulders, "innovation" and "exploration" may become luxuries. Whether this is entirely bullish for crypto remains to be seen.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Asia Bitcoin Summit: Eric Trump on Crypto and Freedom

Trump-backed American Bitcoin Surges 60% in Nasdaq Debut

Smarter Web Company Signs New 21M Share Subscription Agreement

SEC Reviews Quantum Proof Plan For Bitcoin And Ethereum