Suddenly! A sharp plunge across the board, what happened?

The semiconductor sector in Japan and South Korea was hit by a sharp sell-off.

Today, after the opening of the Japanese and South Korean stock markets, chip giants plummeted across the board. Japanese chip testing equipment manufacturer and Nvidia supplier Advantest plunged more than 9% at one point, South Korean equipment manufacturer Hanmi Semiconductor dropped more than 6%, SK Hynix fell more than 5%, and Samsung Electronics tumbled more than 3%. The main reason for the plunge in Japanese and South Korean chip stocks was the sell-off in US tech stocks last Friday.

Some analysts pointed out that the disappointing earnings guidance from some US chip giants triggered concerns in the market about a slowdown in future earnings growth for artificial intelligence (AI) chips. In addition, Nvidia also delivered negative news. According to the latest disclosed data, nearly 40% of Nvidia’s revenue in the second quarter of fiscal year 2026 came from just two customers, sparking discussions in the market about whether Nvidia is overly reliant on a few major clients.

Japanese and South Korean chip stocks plunge

On September 1, chip stocks in the Japanese and South Korean markets plunged across the board. By the close, Advantest plummeted 7.97%, Japanese chip manufacturer Renesas Electronics fell 2.21%, Hanmi Semiconductor dropped 6.32%, SK Hynix fell 4.83%, and Samsung Electronics dropped 3.01%. As a result, the Japanese and South Korean stock markets collectively declined. By the close, the Nikkei 225 Index fell 1.24%, and the Korea Composite Index dropped 1.35%.

Analysts pointed out that the sharp decline in Japanese and South Korean chip stocks was mainly due to the sell-off in US tech stocks last Friday. By the close of that day, the Philadelphia Semiconductor Index had dropped more than 3%, Marvell Technology plunged more than 18%, Oracle fell 5.9%, and Nvidia, Broadcom, TSMC ADR, and AMD all dropped more than 3%. Micron Technology, Applied Materials, ASML ADR, and Intel all fell more than 2%.

Among them, Marvell Technology’s latest earnings report provided guidance that fell short of market expectations, triggering investor concerns about a slowdown in future earnings growth for AI chip concept stocks.

In addition, the “AI leader” Nvidia also showed a warning sign. According to disclosures from the US Securities and Exchange Commission (SEC), nearly 40% of Nvidia’s second-quarter revenue came from just two customers.

Among them, “Customer A” accounted for 23% of total revenue, and “Customer B” accounted for 16%. This proportion is significantly higher than the same period last year, when the top two customers contributed 14% and 11% of sales, respectively. This disclosure once again sparked discussions in the market about whether Nvidia is overly reliant on a few major clients, especially cloud computing giants such as Microsoft, Amazon, Google, and Oracle.

In its financial report, Nvidia did not disclose the specific identities of Customer A and Customer B. Nvidia pointed out that these are all direct customers, including original equipment manufacturers (OEMs), system integrators, or distributors who purchase chips directly from Nvidia. Indirect customers, such as cloud service providers or consumer network companies, purchase Nvidia chips from these direct customers.

Wall Street analysts pointed out that although highly concentrated revenue among a few customers brings risks, these customers have ample cash and large free cash flows, and are expected to continue investing heavily in data center construction in the coming years.

The risk of high valuations

Wall Street institutions believe that the root cause of the sharp fluctuations in US AI chip concept stocks lies in the previously accumulated excessively high expectations and very high valuations, leaving almost no room for error in the financial reports of related listed companies.

It is worth noting that the overall valuation of the US stock market has reached an unprecedented level, even surpassing the peak of the dot-com bubble era.

According to the latest data, the price-to-sales ratio of the S&P 500 Index has reached 3.23 times, a record high. In addition, the S&P 500 Index’s price-to-earnings ratio based on expected earnings for the next 12 months is 22.5 times, far higher than the average of 16.8 times since 2000.

Some analysts pointed out that the record-high valuation of US stocks is mainly driven by tech giants such as Nvidia and Microsoft. According to Morningstar data, as of the end of July, the 10 largest companies in the S&P 500 Index accounted for 39.5% of the index’s total market capitalization, the highest level on record.

Steve Sosnick, chief strategist at Interactive Brokers, warned that the combination of extremely high valuations and very crowded trades undoubtedly increases the likelihood of a sharp decline in the US stock market.

Data shows that ordinary companies in the S&P 500 Index are not significantly overvalued. If each company in the S&P 500 Index is given equal weight, rather than being weighted by market capitalization, the equal-weighted index’s price-to-sales ratio would be 1.76 times, not much different from its long-term average of 1.43 times.

As for whether US tech giants can maintain their current high valuations in the long term, some market participants are skeptical. They believe that over time, fundamentals and valuations will ultimately become the key factors determining stock prices.

Mark Giambrone, head of US equities at Barrow Hanley Global Investors, said: “Valuations will eventually matter, and the expectations embedded in these valuations are also crucial. Right now, those expectations are becoming so high that companies will find it very difficult to meet them.”

Meanwhile, warnings about an AI bubble are becoming more frequent. Following OpenAI founder and CEO Sam Altman, Grindr CEO George Arison has stated that an “AI venture capital bubble” is forming.

In a recent interview, Arison warned: “Due to the venture capital frenzy for AI, many great companies will be destroyed.” He compared it to the investments made by Japan’s SoftBank Group in the late 2010s.

Arison cited as examples that SoftBank Group invested $9 billion in WeWork, which later filed for bankruptcy. It also invested $375 million in Zume, which has now shut down.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin valuation indicator hints at macro top as ‘death cross’ appears

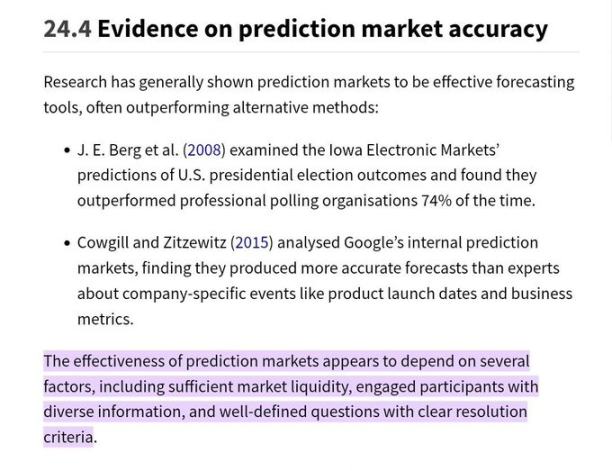

If the next major opportunity comes from prediction markets, how should we choose the most promising platform?

A platform with sound mechanisms, ample liquidity, and a vibrant, trustworthy community is more likely to provide value in terms of profitable trading opportunities and accurate predictions.

Dark Forest Adventure Round: A New Era of On-Chain Economy with AI Agents

Building an on-chain gaming financial market to empower AI agents for sustainable profitability.

The Art of War in Crypto: Winning the Psychological Battle Is the Best Marketing

Today's crypto marketing is not just about advertising; it's a series of psychological battles.