USDC Ownership Battle: Why Did Coinbase Ultimately Have to Acquire Circle?

Coinbase is expected and very likely to acquire Circle.

Original Article Title: Coinbase Will Have to Acquire Circle – The Only Question Is Price

Original Article Author: Ryan Y. Yi

Original Article Translator: Deep Tide TechFlow

Background

I have been deeply involved in the cryptocurrency industry for many years—having worked at early-stage fund CoinFund and later at Coinbase, helping expand its venture capital strategy. All the analysis in this article is based on public data, including Circle's S-1 filing (April 2025) and Coinbase's public financial files. There is no insider information involved, just analysis that anyone could do but most have not.

USDC Supply Structure Analysis

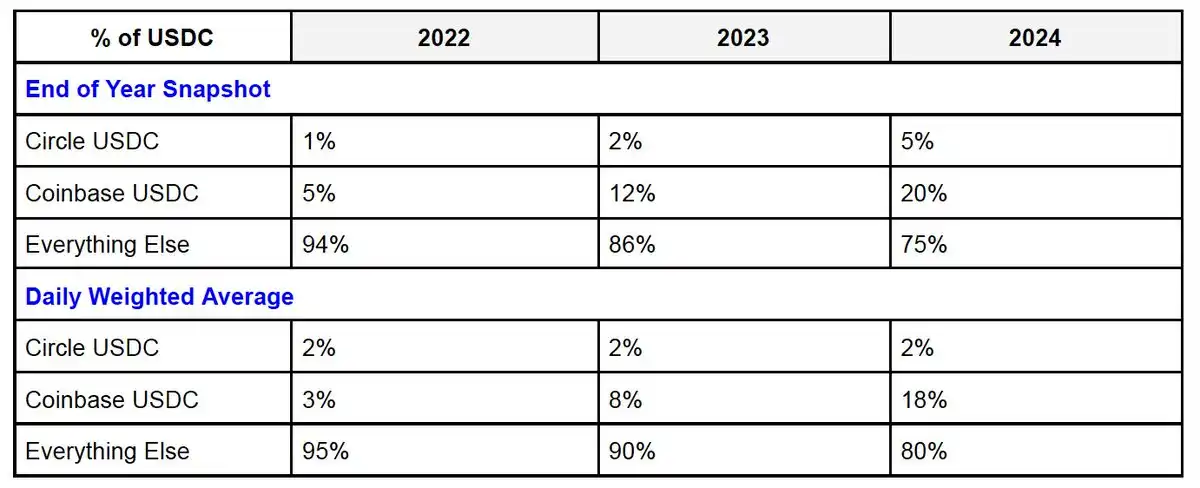

The total USDC supply can be divided into three parts: Coinbase's USDC, Circle's USDC, and USDC on other platforms. According to Circle's S-1 filing, "Platform USDC" refers to "the share of the stablecoin held in a wallet service or managed product by a counterparty." Specifically:

· Coinbase: Includes USDC held by Coinbase Prime and the exchange.

· Circle: Includes USDC held by Circle Mint.

· Other platforms: Such as Uniswap, Morpho, Phantom, and other decentralized platforms holding USDC.

Coinbase's share of the total USDC supply is rapidly growing, reaching about 23% in the first quarter of 2025. In contrast, Circle's share has remained stable. This trend reflects Coinbase's stronger influence in the consumer, developer, and institutional markets.

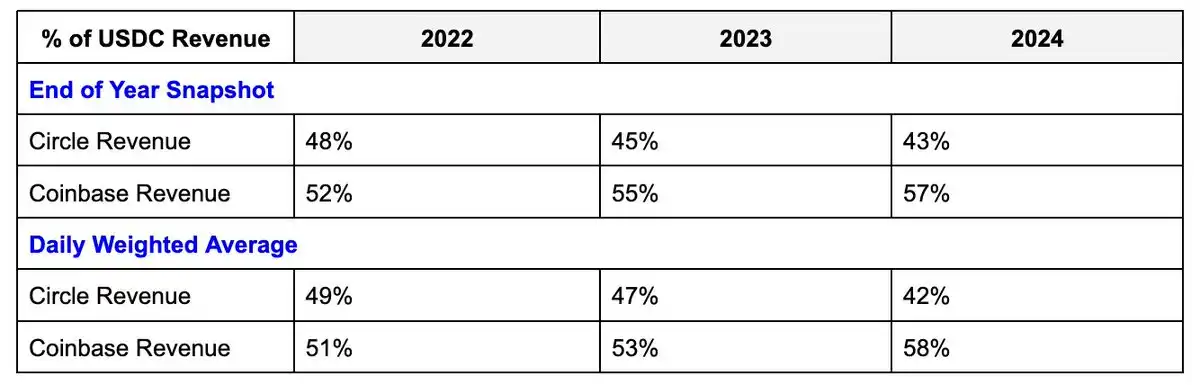

USDC Revenue Distribution

For USDC on their platforms, Circle and Coinbase each retain 100% of the reserve revenue. However, for USDC off their platforms (i.e., the "other platforms" part), they split it 50/50. But there is a key point here: Circle benefits more from the USDC pool off the platform. Despite Coinbase having four times the amount of USDC on its platform compared to Circle, its revenue advantage is only about 1.3 times that of Circle. Some rough calculations based on a 50-50 split of the "other" part yield the following revenue distribution results:

Circle: Betting on Market Size Rather Than Control

Circle's motivation is clear: to drive the total circulation of USDC, even if that USDC is not held on its own platform. For Circle, the ideal scenario is for USDC to become the preferred stablecoin, a result that is defensive and competitive in itself. As the underlying protocol provider for USDC, Circle has the following advantages:

· Publishing and maintaining USDC smart contracts on more than 19 blockchains.

· Controlling the Cross-Chain Transfer Protocol (CCTP) native bridging and minting/burning processes.

· While the profitability of USDC on the platform is higher, its growth is not significant. In high-risk business expansion, Circle's scale is often not as large as Coinbase's. However, if USDC ultimately becomes the No.1 USD stablecoin, Circle will still emerge as a winner. This is a game based on Total Addressable Market (TAM) rather than profit margin competition.

· The potential market size of USDC may be large enough to render these details less important—most of Circle's revenue growth is expected to come from the "other platforms" segment (which is not a bad outcome). This motivation aligns with Circle's capabilities as Circle controls USDC governance, infrastructure, and technical roadmap.

Coinbase: Must Fully Control USDC

Macro View

USDC is Coinbase's second-largest revenue source, accounting for approximately 15% of Q1 2025 revenue, surpassing staking revenue. It is also one of Coinbase's most stable and scalable infrastructure revenue sources. With USDC's global expansion, its potential returns are asymmetric. In the future, USDC will become Coinbase's core business and build its competitive moat. Although Coinbase's primary revenue source remains transaction volume revenue from centralized exchanges (CEX) and will continue to grow with market expansion, USDC's revenue model is more stable and will steadily grow with the overall development of the crypto economy.

USDC will rise to the top three USD stablecoins and become a technology-driven solution for global dollarization. Leaders in fintech and traditional finance have already recognized this, which is why they are taking action. However, USDC, with its early market advantage and support from the crypto economy, has the ability to survive and grow in competition. From an infrastructure and regulatory perspective, full control of USDC is a highly valuable narrative.

Micro Perspective: Coinbase's Profitability Dilemma

Coinbase is a key driver of USDC growth but faces structural limitations. USDC has now become Coinbase's second-largest revenue stream, just behind trading revenue and ahead of staking revenue. Therefore, every product decision at Coinbase needs to be balanced from a revenue and profit perspective. The core issue is that while Coinbase has expanded the Total Addressable Market (TAM), it has not fully captured the revenue. As the market size expands, it needs to share the earnings with Circle—receiving only a 50% cut of off-platform revenue.

Ironically, Coinbase is actively working to boost the USDC ecosystem—attracting users, building infrastructure, and improving transaction speeds—yet it faces structural limitations on revenue. Its consumer and developer products have been "hollowed out" from the start.

Coinbase's natural response is to convert market size into "Coinbase USDC," a fully monetizable portion—such as balances stored in custody products, allowing Coinbase to capture 100% of reserve revenue. This strategy has proven successful: over the past two years, the proportion of USDC on the Coinbase platform has grown fourfold. However, this strategy only applies to custody-based USDC, specifically for exchanges and the Prime product line. The issue arises in the gray area of custody—where growth happens but revenue ownership becomes murky.

For example:

· Coinbase Wallet: Being by definition a non-custodial wallet, despite its smart wallet enhancements to user experience and potentially introducing a shared key model, it may still not meet the definition of "platform USDC" in the S-1 filing. If a majority of users interact with on-chain products in this way in the future, a significant amount of USDC held by consumers will fall into the revenue attribution gray area between Coinbase and Circle.

· Base (Coinbase's Layer 2 network): With a non-custodial architecture where users can independently exit to Ethereum L1, Coinbase does not hold the keys. Any USDC on Base may not be counted as "Coinbase USDC" as per the S-1 definition, even if Coinbase is, in fact, the primary on-ramp to Base.

· Key Takeaway: Coinbase's growth in consumer and developer products has driven USDC usage but has embedded a "hollowing out system." Unless Coinbase can control the protocol layer of USDC, it will always face revenue attribution uncertainty. The only definitive solution is to directly acquire Circle and redefine the rules.

Key Benefits of Acquiring Circle

100% Revenue Ownership

Post the acquisition of Circle, Coinbase will no longer be constrained by the custody vs. non-custody legal definition debate. It can outright claim full ownership of all interest income generated by USDC—regardless of where USDC is held, gaining access to the entire interest income of the approximately $60 billion USDC reserve. The custody definition dispute will no longer exist, and Coinbase will have complete control over all USDC interest income.

Protocol Control

The USDC smart contract, multi-chain integrations, and Cross-Chain Transfer Protocol (CCTP) will all become internal assets of Coinbase. This means Coinbase will have full control over the technical infrastructure of USDC.

Strategic Product Advantage

Post-acquisition, Coinbase can natively monetize USDC in wallets, Base (Layer 2 network), and future on-chain user experiences without the need to coordinate with third parties. USDC can serve as an abstraction layer for future on-chain interactions, with this integration not requiring third-party approval.

Regulatory Integration

As a leader in the crypto policy space, Coinbase, by controlling USDC, can shape stablecoin regulatory rules from the top. Mastering the core technology and operational rights of a stablecoin will give Coinbase more leverage in regulatory negotiations.

Uncharted Territory and Unresolved Issues

Growth Potential

The current market cap of USDC is around $60 billion, but it is expected to reach $500 billion in the future, corresponding to approximately $20 billion in annual reserve income. This will make USDC a core driver for Coinbase to achieve "Mag7" status (revenue level of top global tech companies).

Regulatory Factors

The US is advancing stablecoin legislation (GENIUS Act), which, from a macro perspective, is bullish for the upper growth of stablecoins as it embeds stablecoins deeply into the existing US financial system. Additionally, stablecoins will become a tool for the global dominance of the US dollar. However, this may also lead to traditional financial institutions (TradFi) and fintech companies entering the market as stablecoin issuers. Furthermore, related regulations may restrict platforms' marketing of income or savings products. Acquiring Circle will provide Coinbase with the flexibility to adjust its direction and marketing strategies to adapt to the evolving regulatory landscape.

Operational Challenge

USDC was initially designed in a consortium model, which may have been based on legal and regulatory considerations at the time. Although these obstacles should be overcome within a single company framework, it is currently unclear where the specific red lines of these complex mechanisms lie. Deconstructing the existing legal structure may bring edge case risks, but as of now, these risks appear to be surmountable.

Price

Market outcomes are never perfectly predictable, but we can refer to some disclosed data:

· Circle is seeking to go public with a valuation of $50 billion.

· Ripple's IPO valuation target is $100 billion.

· Coinbase's current market value is around $70 billion.

· USDC currently accounts for approximately 15% of Coinbase's revenue, with the potential to exceed 30% if fully integrated.

Personal interpretation:

· Based on the above data, Circle is a natural acquisition target for Coinbase, and Coinbase is well aware of this.

· Circle aims to have the market value them through an IPO (targeting $50 billion).

· Coinbase, on the other hand, wants to observe how the market prices Circle.

Coinbase may have realized the following:

· For the aforementioned reasons, Coinbase needs full control of USDC's entire stack business.

· Full ownership of USDC could increase its revenue share from the current 15% to between 15% and 30%.

· From a revenue's 1:1 valuation perspective, USDC's ownership could be priced between $100 billion and $200 billion.

Circle may also be well aware of this—they know that if the market values them high enough and USDC continues to grow, Coinbase will be more motivated to acquire Circle directly, to rid themselves of various cumbersome issues with third-party partners in business, product, and governance, and to integrate them into Coinbase's system.

Final Conclusion

Coinbase should and is likely to acquire Circle. While the current partnership model is functioning well, the conflicts on platform, product, and governance fronts are too significant to ignore in the long run. The market will price Circle, but both parties already have a clear understanding of each other's value.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Render (RENDER) To Rise Higher? Key Harmonic Pattern Signals Potential Upside Move

Shiba Inu Price Prediction: SHIB Coin Preparing for a 60% Breakout

DOGE News Today: Elon Musk Exit, Congress Cuts, and Price Surge to $1?